A number of readers have asked me what I think about Paul Merriman’s Ultimate Buy-and-Hold Portfolio. It sure does have a nice ring to it (placing the word “ultimate” before anything tends to have that effect). Merriman believes that you can increase the expected return of a simple Couch Potato portfolio by adding more small-cap and value companies to the mix. This is not a new idea – for decades now, academics have known about the historical small-cap and value premiums. Notable fund companies, like Dimensional Fund Advisors (DFA), have even created products based on their research.

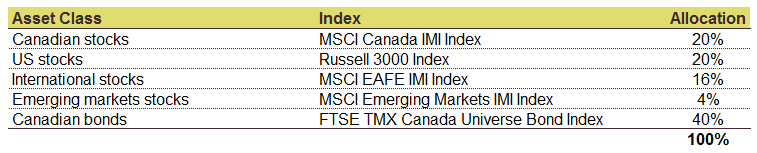

Although Merriman’s articles are written from a US perspective, we can take his concepts and apply a Canadian spin to them. First, let’s take a look at a balanced Couch Potato portfolio (similar to my 40FI-60EQ model ETF portfolio). You can see that the equity mix is made up of 20% Canadian stocks, 20% US stocks, 16% international stocks and 4% emerging markets stocks.

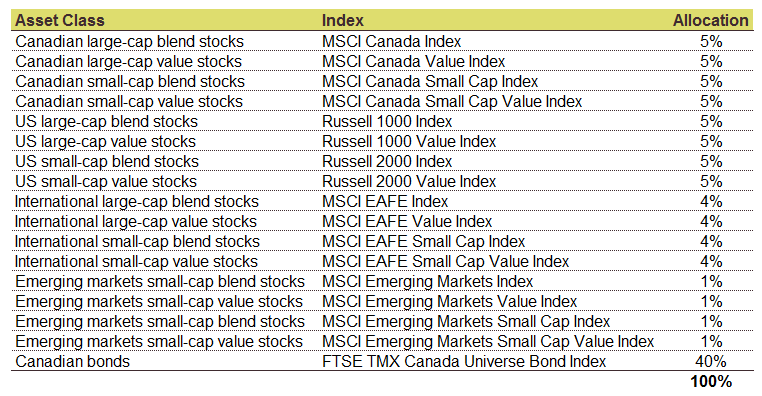

We’ll then divide each equity region into four equal parts, consisting of large-cap blend, large-cap value, small-cap blend and small-cap value companies. Merriman usually includes real estate investment trusts (REITs) in his model portfolios as well, but I’ve excluded them so that we can view the small-cap and value effects in isolation).

Portfolios are rebalanced annually

Portfolios are rebalanced annually

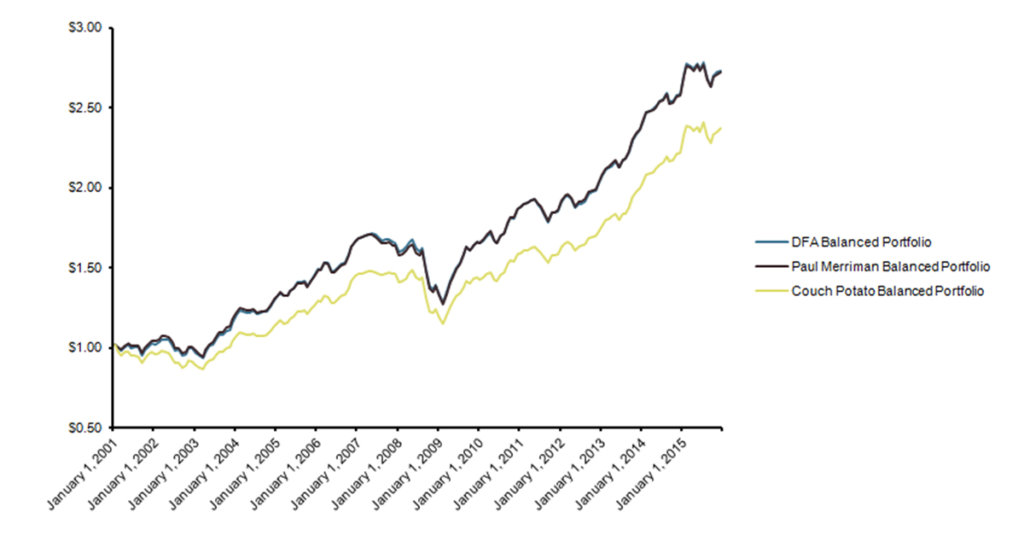

Comparing the performance of the two portfolios, we find that the Couch Potato portfolio has outperformed the Merriman portfolio over the 1, 3 and 5 year periods ending December 31, 2015. Both portfolios performed similarly over 10 years. The Merriman portfolio started to shine after 15 years, beating the Couch Potato portfolio on average by about 1% each year.

There are a few insights that can be gained from this example. First, 15 years is a long time to wait for higher expected returns (with absolutely no guarantee of higher returns than the index). There is a huge behavioural argument against straying from the index for any active strategy.

Second, Merriman’s portfolio is much more complex than the Couch Potato portfolio. It contains 12 additional holdings, which must be managed as new cash is added to the portfolio and rebalancing opportunities arise. ETFs that have a similar value and small-cap tilt may not even be available to DIY investors.

Third, these figures are before any fees or taxes. If Merriman’s portfolio could be theoretically constructed using readily available ETFs, the ongoing costs would likely be higher than a Couch Potato portfolio.

For DIY investors, I always recommend keeping things simple and sticking with a Couch Potato portfolio. Trying to piece together the necessary ETF parts like a mad scientist could result in a portfolio abomination. Much like Victor Frankenstein, you may end up abandoning your monster shortly after its creation.

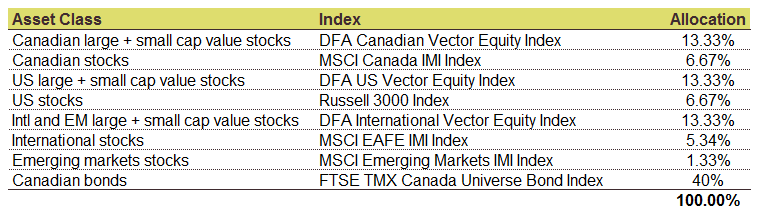

If you have an advisor that has access to DFA funds, there is a relatively easy way to create a Paul Merriman portfolio. For each equity region, simply have your advisor mix about 1 part broad-market ETFs with 2 parts DFA Vector Funds – by doing this, you’ll end up with a decent Merriman clone. I’ve included the weights of the indices below – you’ll notice these are very similar to the model DFA portfolios that some of our clients invest in.

The DFA portfolio performance below is nearly identical to the Merriman portfolio performance. I’ve also included an additional graph showing the growth of $1 for each of the portfolios. The blue line representing the DFA portfolio is barely distinguishable from the brown line representing the Merriman portfolio.