One of the most complicated and tedious tasks you get to do as an investor is to calculate the adjusted cost base (or ACB) for each security in your taxable accounts. Let’s just say, keeping track of your ACBs is NOT as easy as learning your ABCs … but it’s every bit as essential as far as your ETF investments are concerned.

So, how do you do it? You start with the original cost of your investment. Then, you adjust your base upwards for any new purchases – such as lump-sum buys, dividend reinvestment plans, or reinvested distributions. You also adjust it downwards for any sells, or return of capital distributions.

While calculating your securities’ ACBs is complex and time-consuming, it’s also extremely important. If you don’t adjust them upwards, you’ll pay too much tax when you sell a security. If you neglect to adjust them downwards, you’ll pay too little. That part may sound appealing, but the Canada Revenue Agency is not likely to share your enthusiasm.

Like it or not, if you are a do-it-yourself ETF investor, accurately tracking your adjusted cost bases, or ACBs, is ultimately your privilege and responsibility. It would be nice if your brokerage did it for you. Unfortunately, you can’t count on that, and your brokerages are not entirely to blame: Because your ACBs must be calculated for identical securities across all your taxable accounts, no single brokerage can see your entire picture.

That said, while your brokerages can only help so much, you do have our sympathies here at Canadian Portfolio Manager … along with today’s video/blog combo to make it easier for you.

Are you ready to dive in?

First, let’s talk about the timing. We recommend completing your ACB record-keeping tasks annually, every March, before you file your personal tax return. By then, ETF providers should have had enough time to report the tax breakdown of their funds’ distributions, which factor into your ACB calculations.

Your first step is compiling all the required information from your monthly or quarterly non-registered account statements. (Remember, it’s not necessary to track your ACBs for securities held in TFSAs, RRSPs or other registered accounts).

Focus on the account activity section of each statement: This will include any buys or sells that took place during the calendar year, plus any dividend reinvestment plans, or DRIPs.

Let’s illustrate. Imagine you invested in the Vanguard Growth ETF Portfolio (VGRO) on January 3, 2020, and sold it on January 29, 2021. Along the way, there were six relevant transactions. First, there was the buy, settling on January 3. Then there were four DRIPs: Three of them settled in April, July, and October 2020, and one more settled in early January 2021. Finally, on January 29, you sold your VGRO units.

So far, so good. Next, we’ll obtain the tax breakdown for all ETF distributions recorded during the calendar year. CDS.ca provides an online resource that allows Canadian investors to download tax breakdown spreadsheets for their ETF distributions. These spreadsheets include return of capital and reinvested distribution breakdowns that help you calculate your ACB.

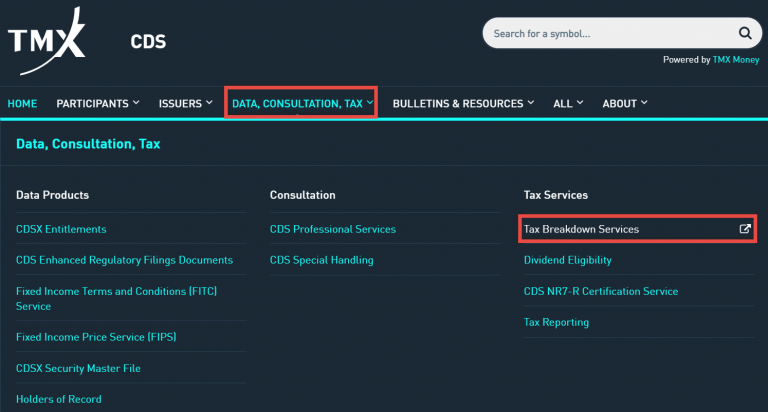

When you visit the website, hover over the DATA, CONSULTATION, TAX tab, and then click on the Tax Breakdown Services option.

Click the link Display tax information for year 2020 (or whichever year you’re working on) and accept the conditions on the Terms of Access, Disclaimer and Legal Information page.

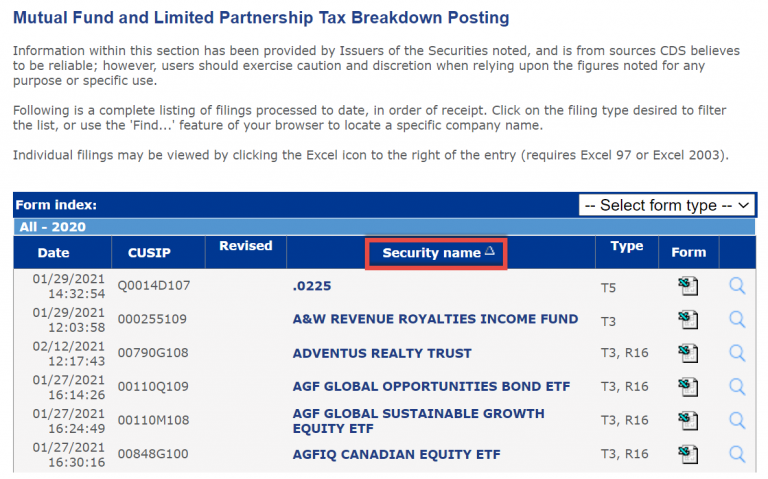

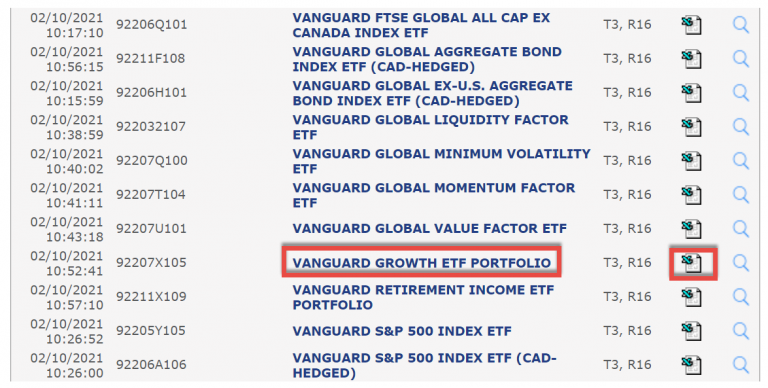

You will then be brought to the Mutual Fund and Limited Partnership Tax Breakdown Posting page. You can sort the funds alphabetically by clicking on the Security name heading. Scroll until you find your ETF, then click on the Excel icon to the right of the fund name. If there are multiple entries with the same name, click on the Excel icon with an “R” to the left of the name. (The “r” indicates a revised tax breakdown).

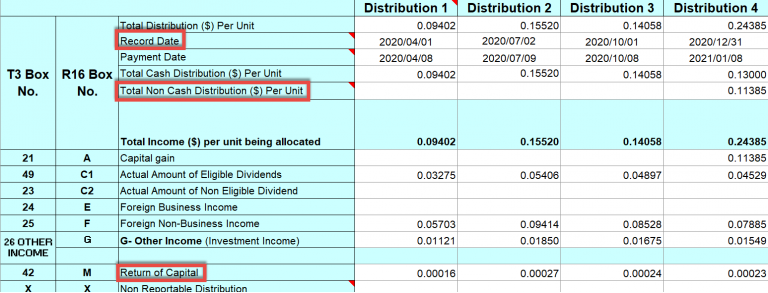

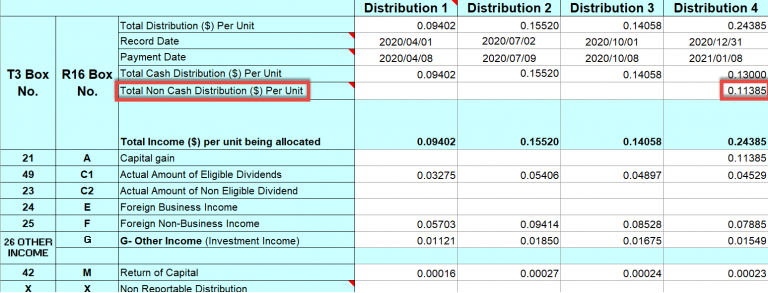

Once you’ve got your spreadsheet, look on the Statement of Trust Income Allocations and Designations for three key pieces of information you may need to calculate and track your ACB. These include: (1) the Record Date, (2) the Total Non Cash Distribution ($) Per Unit, and (3) your Return of Capital.

We recommend saving a copy of this spreadsheet for your tax records.

Now that you’ve armed yourself with all the necessary information to calculate your ACB, it’s time to turn to a free online resource that will do some of the heavy lifting for you.

Adjusted Cost Base.ca allows you to set up an account using only your email address. You can then input and track all buys, DRIPs, sells, reinvested distributions, and return of capital. You can also export this info to Microsoft Excel and download it for your files. (Unless you trust the Internet entirely, we strongly recommend you do so after each annual update, so you’ll always have a backup.)

To get started with Adjusted Cost Base.ca, the first step is to read and agree to the Terms of Use, and register with your email address. Easy enough.

Once you’ve registered and logged into the site, add the name of each ETF you hold in your non-registered accounts. To do this, click on “New Security” at the top of the page.

From there, you will be brought to a separate screen where you can input the ETF name and ticker symbol. For today’s illustration, we’ve entered the Vanguard Growth ETF Portfolio in the “Name” field and VGRO in the “Ticker Symbol” field. Click the “Add Security” button to complete the process.

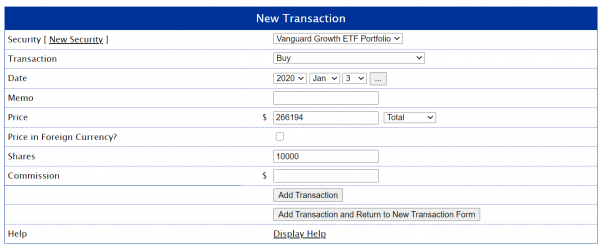

Buying shares of an ETF increases the ACB by the cost of the shares, plus any trading commissions. To input all of your share purchases, click New Transaction at the top of the page:

You will be brought to a separate screen that will allow you to input your transactions.

Select the Vanguard Growth ETF Portfolio from the Security drop-down menu. Choose the transaction type. (In this example, you’d select Buy.) Then select the settlement date of the trade. In today’s illustration, that would be January 3, 2020.

We’ll then enter $266,194 in the “Price” field. This was the total cost of our initial buy, including commissions. You also have the option of selecting “Total” or “Per Share.” Choose “Total” for any buy transactions. You can skip the “Commission” field, as the commission (if any) has already been included in the total cost of the trade.

Finally, input the total number of shares purchased. (In our example, that’s 10,000 shares.) We’ll then click “Add Transaction.”

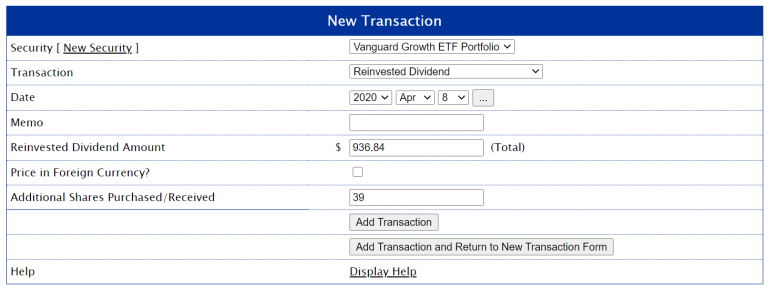

Now, on to our dividend reinvestment plan, or DRIPs. These are referred to as Reinvested Dividends in the adjustedcostbase.ca site. Take note! If you neglect to add your DRIP amounts to your ACB, your future capital gains tax liability will be inflated, and you’ll pay more taxes than you need to.

If you have set up a DRIP, most of your ETF distributions will be paid in the form of new shares. (I say “most,” because only whole shares can be purchased, so a portion of each distribution will also be paid in cash.) New shares received through reinvested dividends increase your initial cost base and lower your future capital gains tax liability.

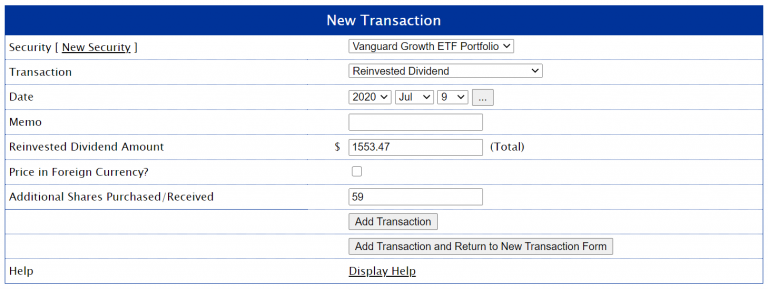

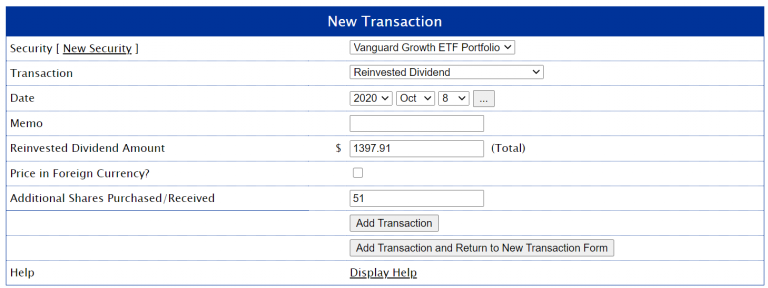

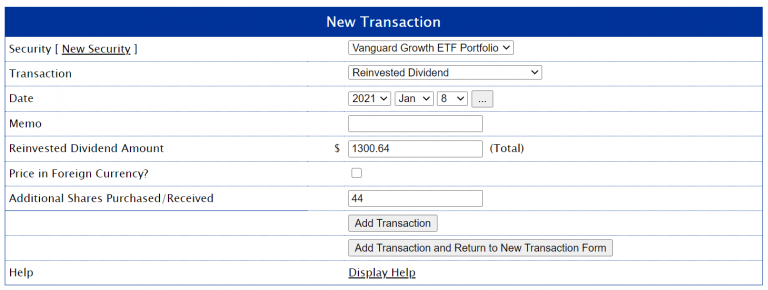

In our VGRO example, there were four DRIP transactions. The first DRIP settled on April 8, 2020, with a reinvested dividend amount of $936.84. This resulted in 39 new VGRO units purchased. To include this information, click on “Add Transaction”, and then follow the same steps for the remaining three DRIP transactions on July 9, 2020, October 8, 2020, and January 8, 2021.

Next, there’s that final sale in our illustration. Selling ETF shares decreases your ACB by the number of shares sold, multiplied by the ACB per share.

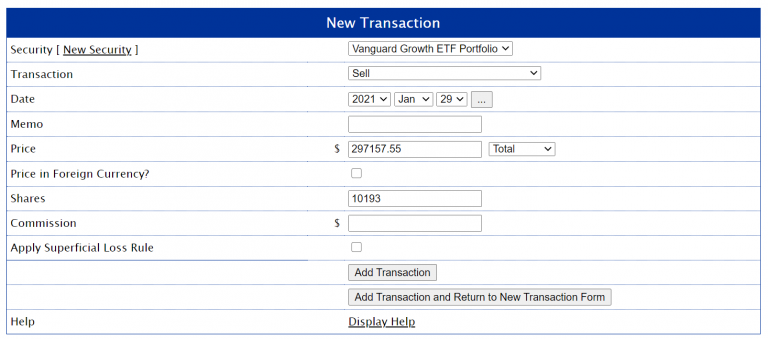

In our example, we’ll again select the Vanguard Growth ETF Portfolio from the Security drop-down menu. We’ll choose the transaction type “Sell,” and then fill in January 29, 2021 as the settlement date of the trade.

We’ll now enter $297,157.55 in the “Price” field. This represents the total proceeds received from the sale, minus commissions. Just as with the “Buy” transaction earlier, you should choose “Total” rather than “Per Share” for any sell transactions, and you can skip the “Commission field,” as we’ve already deducted any commission from the total proceeds received from the sale.

Again, we’ll input the total number of shares sold. In this example, we sold all 10,193 shares. We can then click on “Add Transaction.”

We’re not done yet. Sometimes, fund managers don’t distribute all investment income to their unitholders. They might instead reinvest some of it back into the ETF, which increases your ACB, while decreasing your future capital gains tax liability.

These reinvested distributions often occur annually at year-end. They are generally the result of capital gains realized within the fund. That’s why adjustedcostbase.ca refers to them as “reinvested capital gains distributions.” However, these non-cash distributions aren’t always actual capital gains. They could be the result of a reinvested Canadian eligible dividend distribution, a reinvested return of capital distribution, or any other type of reinvested income distribution. For this reason, I prefer to simply call these non-cash distributions “reinvested distributions”, or “phantom distributions” (since they do not appear on your account statements).

In any case, do not simply add the capital gains figure from box 21 of your T3 slip to your ACB – this could lead to tax reporting errors.

Remember that information I had you download from the CDS.ca website earlier – from its Statement of Trust Income Allocations and Designations? You’ll now use it to accurately calculate reinvested distributions. In the report, find the row labeled Total Non Cash Distribution ($) Per Unit. This is also known as the fund’s reinvested distribution per unit. Each reinvested distribution will be multiplied by the number of units of the ETF held on the record date, and then added to the ACB.

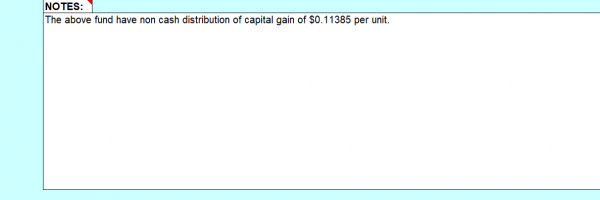

In this example, there was a single 2020 VGRO reinvested distribution of $0.11385 per unit. In the NOTES section of the spreadsheet, Vanguard indicated that this particular non-cash distribution was made up entirely of capital gains.

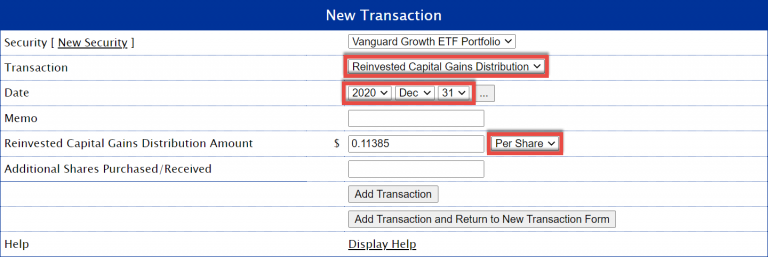

As we held 10,149 units of VGRO on the December 31, 2020 record date, this reinvested distribution will cause our ACB to increase by $1,155.46. That’s 10,149 shares × $0.11385 reinvested distribution per unit. If you fail to make this adjustment, you will pay some unnecessary tax when you eventually sell your VGRO.

To include this reinvested distribution, add a new transaction for VGRO, this time selecting “Reinvested Capital Gains Distribution.” For the “Date” field, use the December 31, 2020 Record Date of the distribution (not the Payment Date).

Then, enter $0.11385 in the “Reinvested Capital Gains Distribution Amount” field. This time, be sure to select “Per Share” instead of “Total” from the drop-down menu to the right. Then click on “Add Transaction.”

There’s one more variation on the theme left to cover. When a fund pays a return of capital, or ROC distribution, it is essentially giving you back a portion of your initial contributions. ROC is not taxable in the year you receive it. However, a return of capital distributions decreases your ACB, which in turn increases your future capital gains tax liability.

If you don’t adjust for return of capital, you will pay less tax than you owe, and the Canada Revenue Agency will not be impressed.

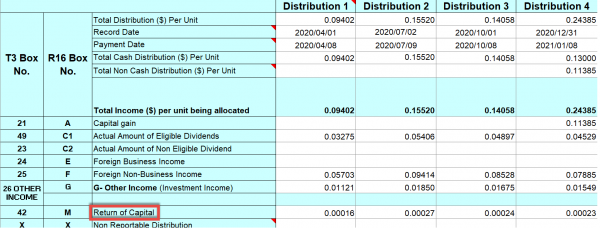

Continuing with the example above, let’s adjust the cost basis by accounting for the return of capital for each year. Again, this information can be found on the Statement of Trust Income Allocations and Designations, in the row labeled “Return of Capital.”

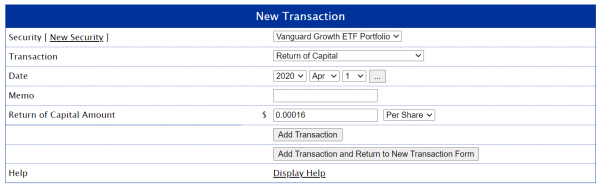

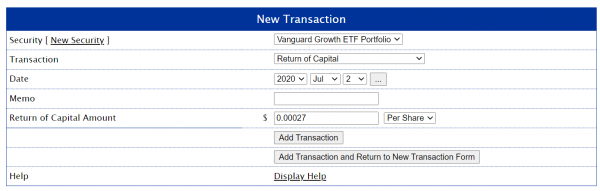

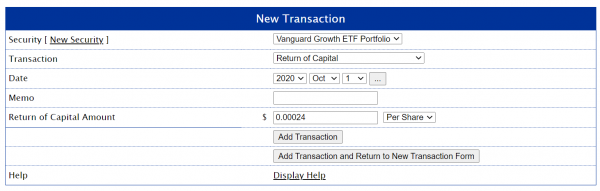

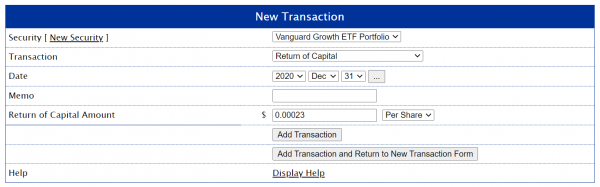

In our VGRO example, there were four quarterly return of capital distributions in 2020. Each of these should be entered as separate transactions.

To include them, add a new transaction for VGRO, this time selecting “Return of Capital.” For the “Date” field, input the April 1, 2020 Record Date of the first distribution (not the Payment Date).

Then, enter $0.00016 in the “Return of Capital Amount” field. Similar to the Reinvested Distribution from our last example, select “Per Share” from the drop-down menu to the right, and click on “Add Transaction.”

Follow the same process for the remaining three return of capital distributions on July 2, October 1, and December 31, 2020.

At last, we’re finished inputting all types of transactions. Now, you can click on “View All Transactions” tab near the top of the screen to review your inputs.

For our VGRO example, we inputted a total of 11 transactions to accurately calculate our ACB and the subsequent capital gain on the full sale of our units. Now, “all” you have to do is complete this same exercise for all your holdings, each year. Hey, don’t look at me, I didn’t make the rules; I’m just showing you how to abide by them!

Again, we also recommend clicking on the “Excel Format” link above your transaction history and downloading a backup copy of the data annually for your records.

Hopefully you now have a better understanding of how to accurately track the adjusted cost base of your Vanguard or iShares Asset Allocation ETF. If you’d like to learn more about calculating your ACBs, check out the white paper I co-authored with Dan Bortolotti.