If you’re a top-rate Canadian taxpayer earning U.S. dividends within your corporation, you’re likely paying a combined corporate-personal tax rate of 57%-67%—which is 10%-15% higher than if you had earned these dividends personally. And for those with a modest income, the additional tax burden could be even greater. In this video, we’ll explore how foreign withholding taxes, along with an imperfect corporate dividend refund process contribute to this issue. We’ll also suggest several strategies business owners can use to mitigate the impact on their bottom line.

Key Concepts

It’s important to note that this issue applies to any foreign dividends subject to withholding tax, including those received from international or emerging markets equity ETFs. However, to simplify our discussion, we’ll focus primarily on U.S. dividends. Also, remember that it’s the withholding tax on foreign dividends—not foreign income in general—that can worsen the situation. If your foreign dividends are exempt from withholding taxes, this is less of an issue.

To help illustrate the tax burden, let’s compare two scenarios:

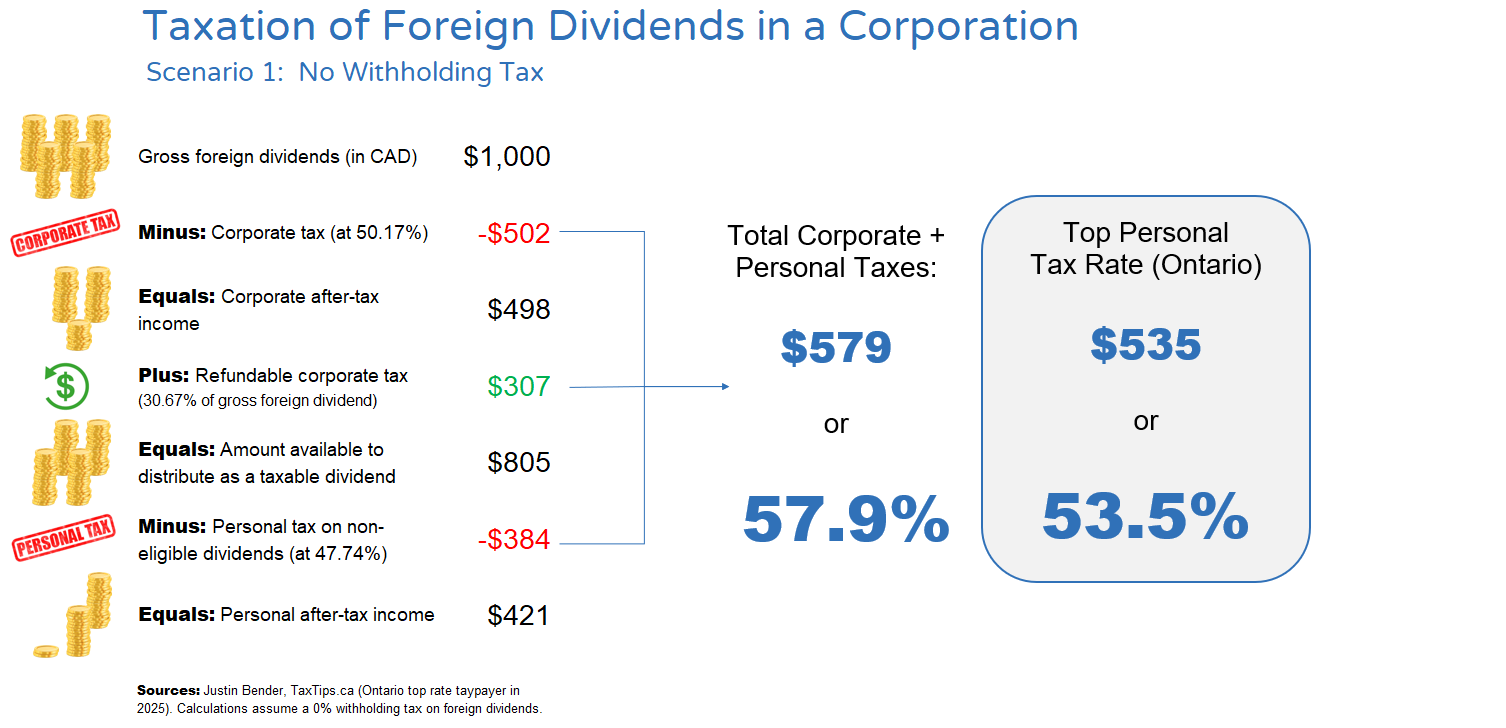

Scenario 1: No Withholding Tax

In the first scenario, let’s assume a top-rate Ontario business owner receives $1,000 CAD of gross U.S. dividends within their corporation in 2025 and then distributes the after-tax income to themselves as a taxable dividend. In this example, we’ll assume no foreign withholding taxes apply.

The foreign dividends are subject to a corporate tax rate on investment income of 50.17%, effectively cutting the gross foreign dividends in half. After paying corporate tax, the business owner has $498 remaining from their $1,000 in gross income. They could then choose to either reinvest this $498 within the corporation or distribute it as a taxable dividend. To understand the full impact of corporate and personal taxes, we’ll assume the business owner distributes the income.

Since the corporation has already paid $502 of tax on these foreign dividends, a portion of the corporate tax is refundable when taxable dividends are distributed to shareholders. This refundable tax is calculated as 30.67% of the gross foreign income. So, on $1,000 of gross foreign income (assuming no withholding taxes), the refundable corporate tax would be $307.

In this case, a total of $805 can be distributed as a taxable dividend, which includes the $498 of after-tax corporate income, plus the $307 of refundable corporate tax.

The $805 is then subject to a top personal non-eligible dividend tax rate of 47.74%, which results in $384 of personal taxes. This leaves the business owner with $421 of after-tax personal income. In this case, the combined corporate and personal taxes (minus the refundable corporate taxes) amount to $579, or 57.9%.

Comparison to Earning the Foreign Dividends Personally

You may notice that this is still a higher overall tax rate compared to an Ontario top-rate taxpayer who earned $1,000 of foreign dividends personally. The personal tax burden in this case would be $535, or 53.53%, which indicates that even income not subject to foreign withholding taxes can still be less efficient when earned in a corporation instead of personally.

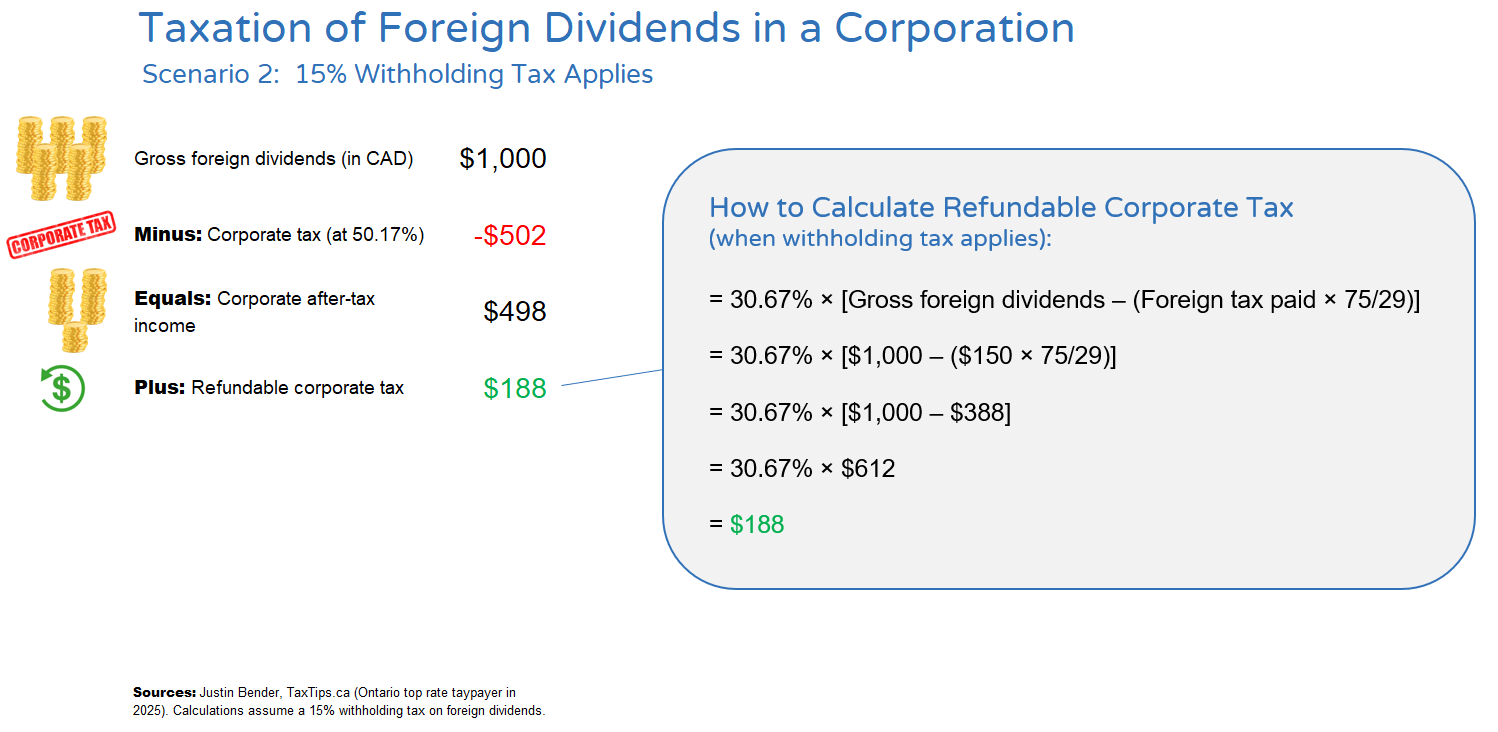

Scenario 2: 15% Withholding Tax Applies

Unfortunately, things get worse when withholding taxes apply to foreign dividends. In this case, a lower portion of the foreign income is eligible for the refundable corporate tax. The reduction is calculated by multiplying the withholding tax paid by 75/29.

For example, let’s assume a 15% U.S. withholding tax on $1,000 of gross U.S. dividends, which would result in $150 of withholding tax. Multiplying $150 by 75/29 gives us $388. We then subtract $388 from the $1,000 gross dividend, leaving $612. This is the final amount that would be multiplied by 30.67% to determine the corporate tax refund of $188.

In other words, withholding taxes reduce the corporate tax refund. The 15% withholding tax rate on the $1,000 gross foreign dividend has reduced the $307 corporate tax refund to only $188.

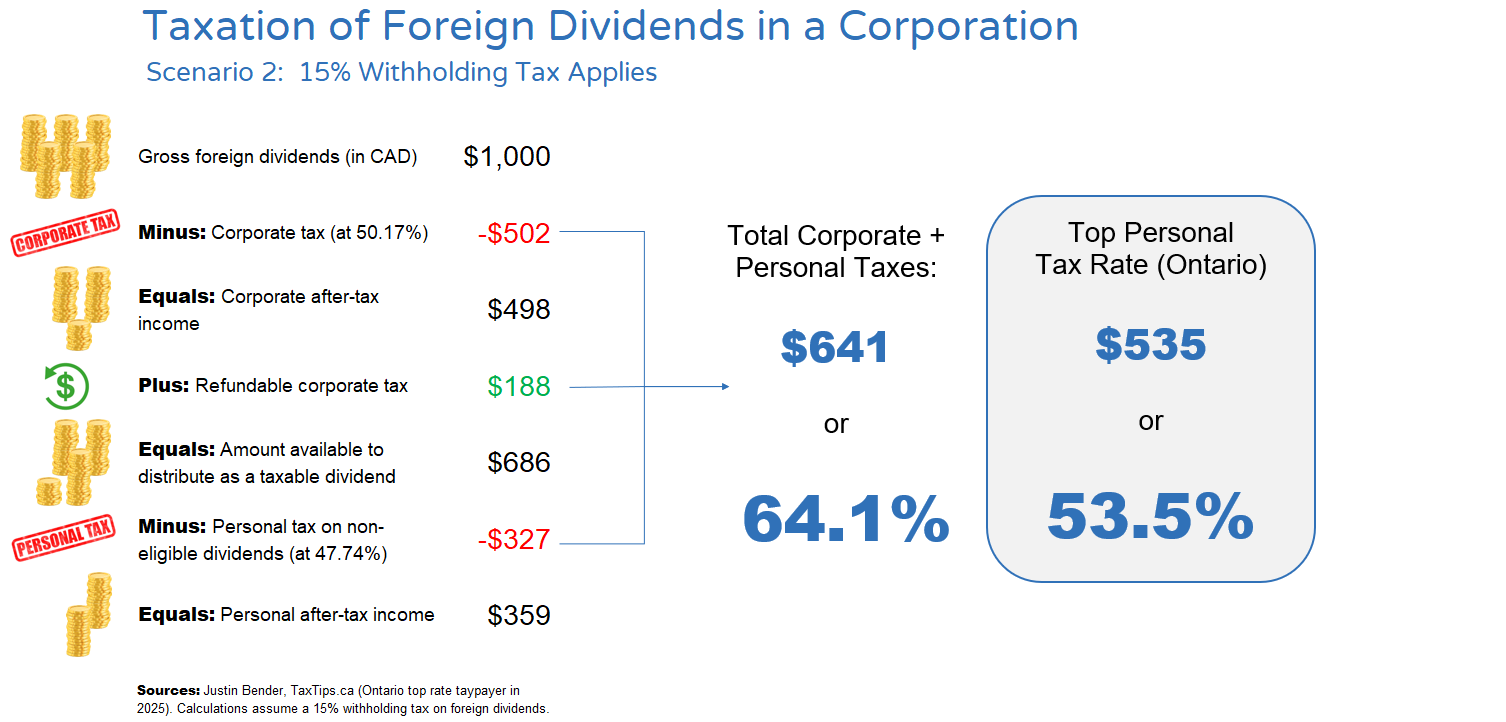

In this scenario, $498 of after-tax corporate income, plus the reduced $188 refund, would be available for distribution to the business owner. After paying additional personal taxes of $327 (47.74% of $686), the business owner would net $359 of after-tax personal income. This results in a combined corporate-personal tax rate of 64.1%—about 10.6% higher than the top personal marginal tax rate of 53.53% in Ontario.

The additional 10.6% tax drag is what we’re referring to when we say that there is a tax disadvantage to earning U.S. dividends in your corporation.

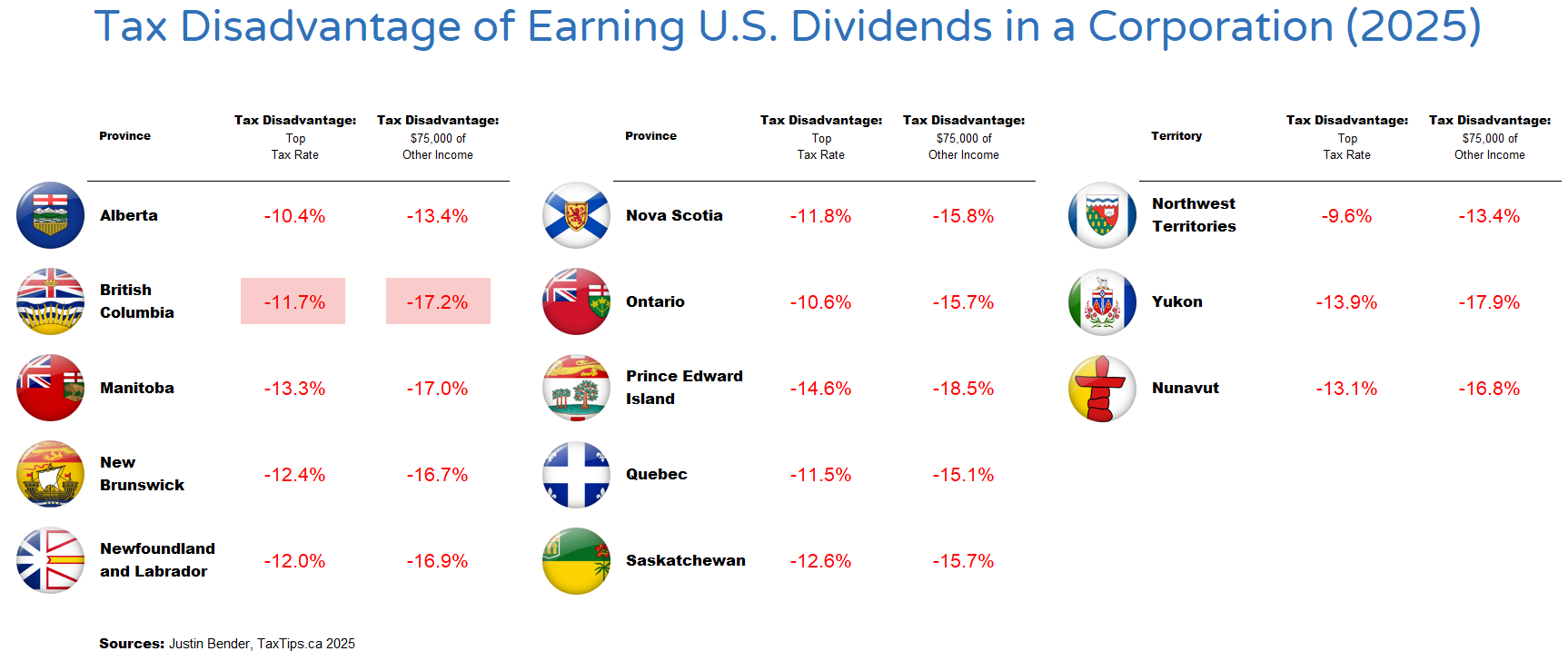

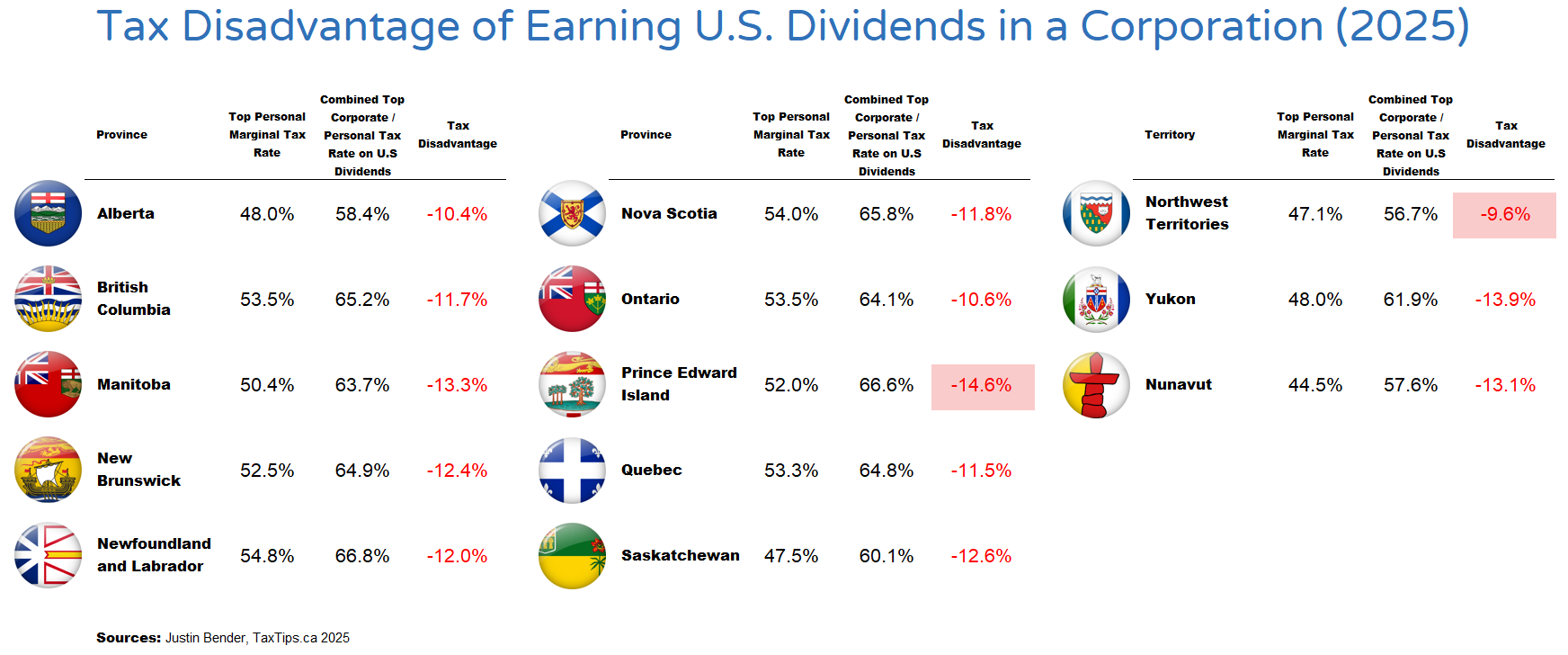

Tax Impact Across Canada

Across Canada, the additional tax drag from earning foreign dividends in a corporation versus personally (assuming a 15% withholding tax rate) ranges from just under 10% in the Northwest Territories to nearly 15% in Prince Edward Island for top-rate taxpayers in 2025.

And at modest personal income levels, this tax inefficiency becomes even more pronounced. For example, in British Columbia, the additional tax drag is around 12% for a top-rate taxpayer but increases to approximately 17% for a taxpayer earning only $75,000 of income.

Strategies to Mitigate the Tax Burden

So armed with this information, how should business owners adjust their portfolios to mitigate the impact?

Increase Your Portfolio’s Allocation to Canadian Stocks

Eligible dividends from Canadian stocks don’t suffer from this tax issue. Therefore, increasing the allocation to Canadian stocks within your portfolio (and specifically, within your corporate account) can improve its tax efficiency. Many all-equity ETFs are already heavily weighted towards Canadian stocks (with 25%-30% allocations being quite common), so your portfolio may already be in good shape. Just be sure you don’t overdo it—diversification should still be a priority.

Use An Asset Location Strategy

You could hold more Canadian stocks in your corporate accounts and more foreign stocks in your personal accounts. This strategy, known as asset location, allows investors to fine-tune the asset classes in each account type for optimal tax efficiency. But be sure you first understand how these decisions could affect the after-tax risk of your portfolio. For a detailed review of asset location strategies, check out my three videos on the topic (which I’ve linked to below).

Justin enjoys sharing his knowledge and skills on his website, Canadian Portfolio Manager, which includes a host of downloadable tools. He has also created a YouTube channel, DIY Investing with Justin Bender, which includes detailed video tutorials for ETF investors.

In this scenario, $498 of after-tax corporate income, plus the reduced $188 refund, would be available for distribution to the business owner. After paying additional personal taxes of $327 (47.74% of $686), the business owner would net $359 of after-tax personal income. This results in a combined corporate-personal tax rate of 64.1%—about 10.6% higher than the top personal marginal tax rate of 53.53% in Ontario.

The additional 10.6% tax drag is what we’re referring to when we say that there is a tax disadvantage to earning U.S. dividends in your corporation.

In this scenario, $498 of after-tax corporate income, plus the reduced $188 refund, would be available for distribution to the business owner. After paying additional personal taxes of $327 (47.74% of $686), the business owner would net $359 of after-tax personal income. This results in a combined corporate-personal tax rate of 64.1%—about 10.6% higher than the top personal marginal tax rate of 53.53% in Ontario.

The additional 10.6% tax drag is what we’re referring to when we say that there is a tax disadvantage to earning U.S. dividends in your corporation.

And at modest personal income levels, this tax inefficiency becomes even more pronounced. For example, in British Columbia, the additional tax drag is around 12% for a top-rate taxpayer but increases to approximately 17% for a taxpayer earning only $75,000 of income.

And at modest personal income levels, this tax inefficiency becomes even more pronounced. For example, in British Columbia, the additional tax drag is around 12% for a top-rate taxpayer but increases to approximately 17% for a taxpayer earning only $75,000 of income.