Unless you were literally born yesterday, you’re probably already aware that 2022 was an extraordinary year for investing … extraordinarily bad, that is. It hardly mattered which asset mix you invested in. Both stock and bond markets experienced double-digit losses, so even conservative investors with bond-heavy holdings saw their portfolio values plummet.

That’s investing for you. We may not like it, but we actually expect some years to serve up heaping helpings of realized risk, sometimes across the board. It’s the price we pay to expect these same markets to deliver longer and stronger runs of future returns.

From this perspective, we hope you’ll keep your eyes and your asset allocations focused on the future as we review the 2022 performance for the Vanguard, iShares, BMO, and Mackenzie asset allocation ETFs.

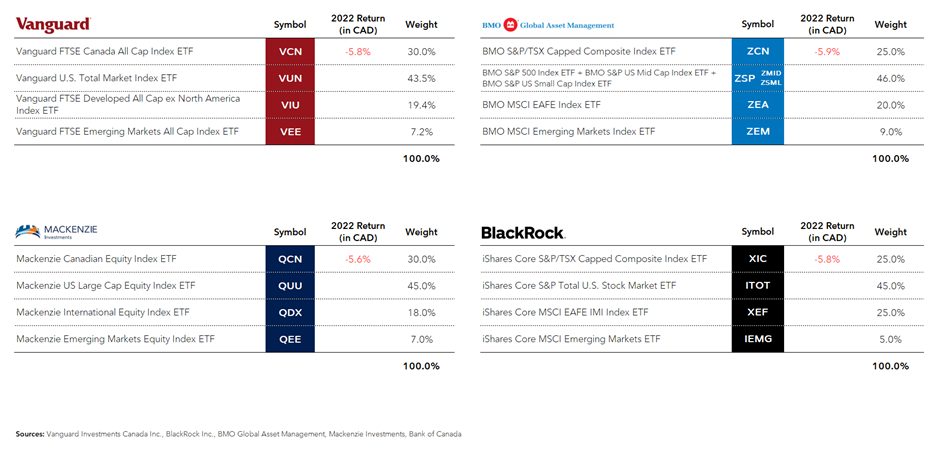

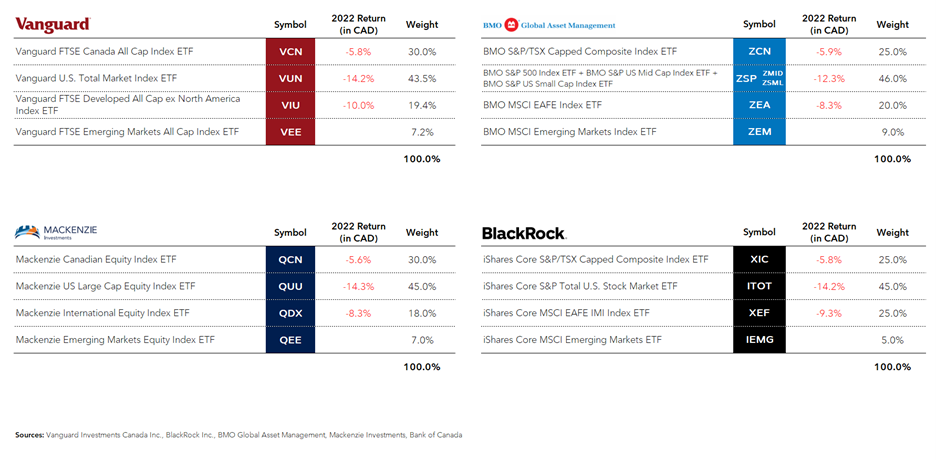

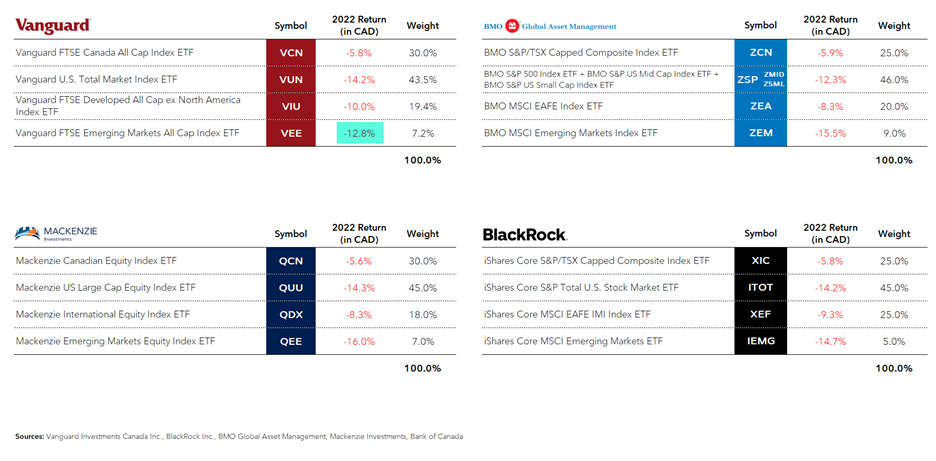

Before we look at the 2022 returns for our asset allocation ETFs, let’s check out the year-end results for their underlying holdings, starting with the equity ETFs.

2022 Equity ETF Returns

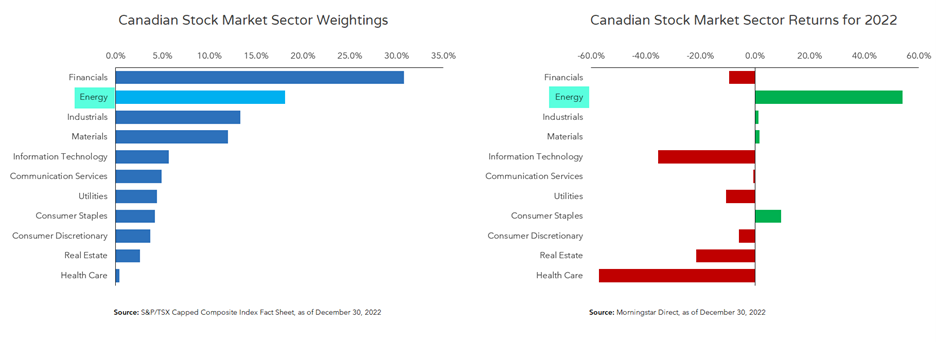

Canadian equity ETF returns were similar across the board, with losses of around 6%.

Disappointing, for sure, but their performance was still better than that of global stock markets, which lost 12% in Canadian dollar terms. That’s in large part due to the Canadian stock market’s overweight to energy companies. The energy sector happened to have a stellar year, returning over 50% during 2022.

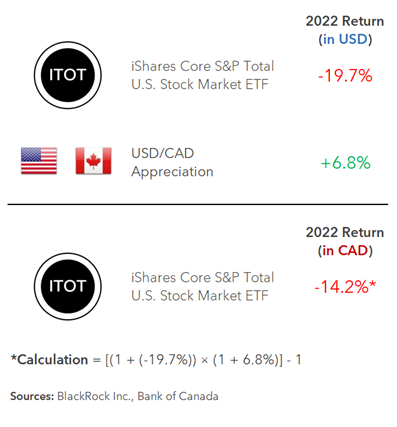

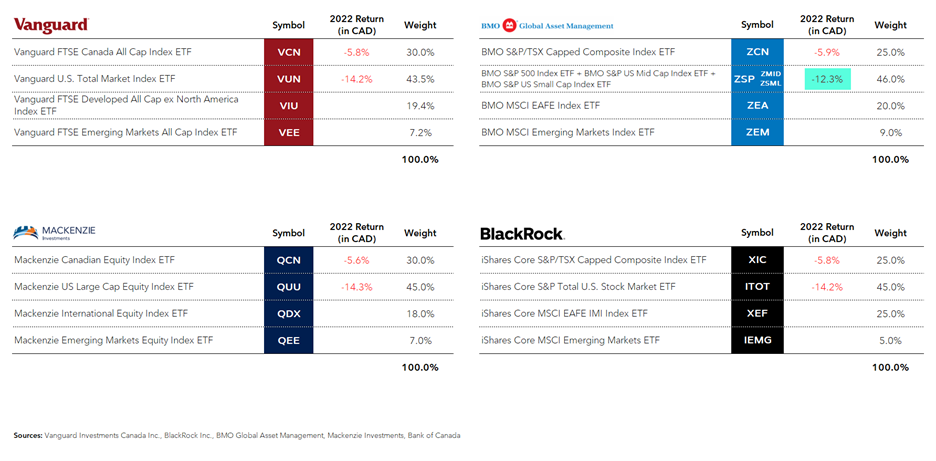

U.S. equity ETFs also ended 2022 on a low note, losing around 20% in U.S. dollar terms. During this time, the U.S. dollar appreciated by 6.8% against the Canadian dollar, reducing the loss for unhedged Canadian investors. Once we factor in the return bump from U.S. dollar exposure, our selection of U.S. equity ETFs lost around 12%-14%, in Canadian dollar terms, net of withholding taxes.

BMO’s trio of U.S. equity ETFs had noticeably higher returns than the others. This is largely due to the methodology used to construct the S&P indexes tracked by BMO’s ETFs. For these indexes, an S&P index committee selects which companies to include in each index. The indexes tracked by the Vanguard, iShares, and Mackenzie ETFs have a less subjective process. This means there is more active decision-making going on in the three S&P indexes tracked by BMO’s ETFs, which led to a wider short-term return difference between BMO and the rest of the more passive index-tracking providers in 2022.

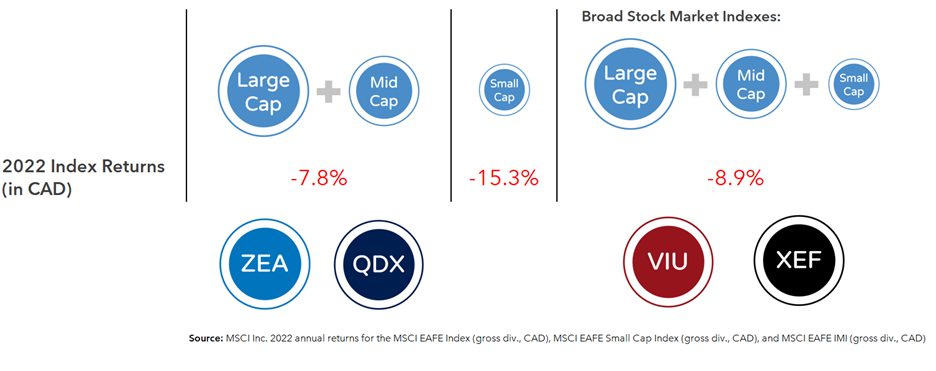

International equity ETFs ended the year on a disappointing note as well, losing between 8%-10%.

Two components explain most of the performance differences among our international ETF providers:

First, small-cap international stocks underperformed relative to their large- and mid-cap counterparts. During 2022, small-cap international stocks lost over 15%, while larger international stocks lost just under 8%. The Vanguard FTSE Developed All Cap ex North America Index ETF (VIU) and the iShares Core MSCI EAFE IMI Index ETF (XEF) follow broad-market indexes, which include large-, mid-, and small-cap stocks. This explains why they underperformed the BMO MSCI EAFE Index ETF (ZEA) and the Mackenzie International Equity Index ETF (QDX), which both exclude small-cap stocks.

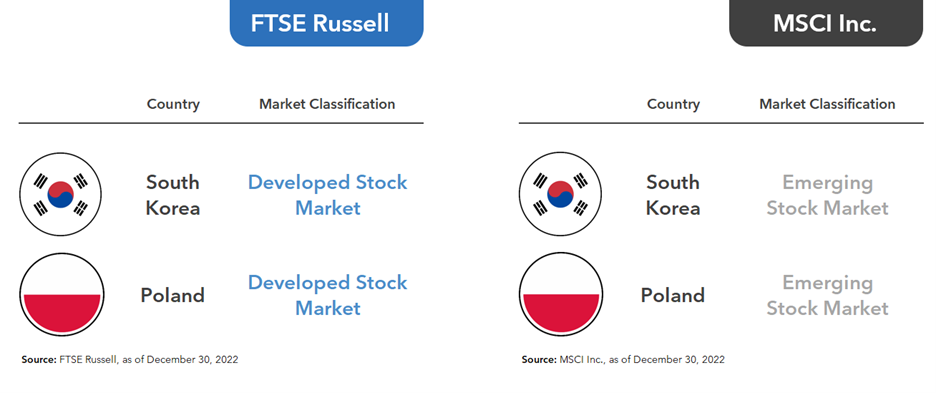

And second, there also were market classification differences among the indexes each ETF follows. This difference can best be seen by comparing VIU and XEF. Because both follow broad market indexes including large-, mid-, and small-cap companies, they offer us a more apples-to-apples comparison.

VIU follows a FTSE index, which classifies South Korea and Poland as developed countries, so VIU includes these countries’ stocks in the fund. XEF follows an MSCI index, which classifies South Korea and Poland as emerging countries, allocating them to MSCI’s emerging markets equity indexes instead.

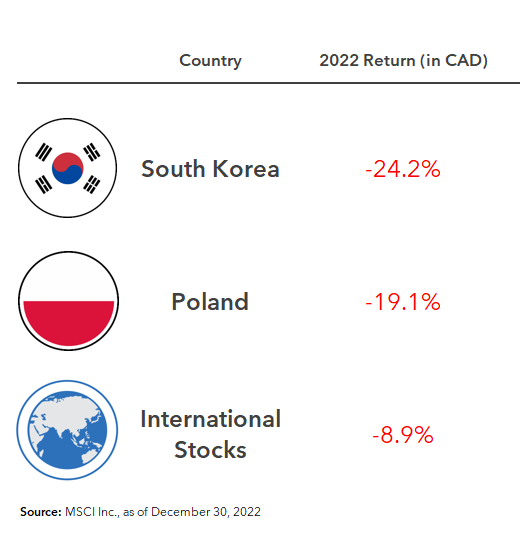

During 2022, South Korean and Polish stock markets lost 24.2% and 19.1%, respectively, in Canadian dollar terms, which was much worse than the overall international stock market. The inclusion of these underperforming South Korean and Polish companies in FTSE’s developed markets indexes reduced VIU’s performance, relative to XEF and the others.

Emerging markets equity ETFs fared the worst among all our asset classes, with negative returns ranging from around 13%-16%. This time, VEE had the slight return advantage over the others, due to its exclusion of the underperforming South Korean and Polish stocks.

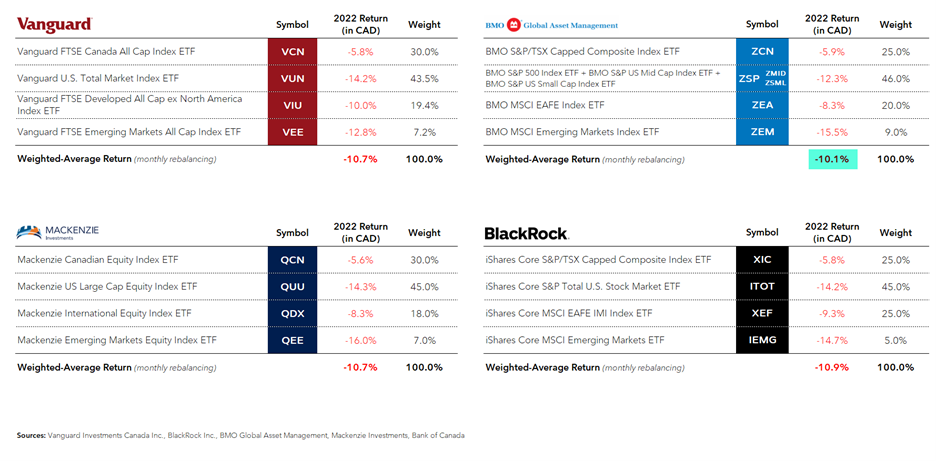

All together now: If we combine these equity asset classes according to their target asset allocation ETF weights, rebalance the portfolios monthly, and adjust for additional product fees, we find their overall equity returns were similar across the board. BMO did manage to slightly outperform the others, with estimated equity returns of around negative 10%. This was a result of their higher U.S. equity ETF returns, along with the small-cap stock exclusion within their international equity allocation.

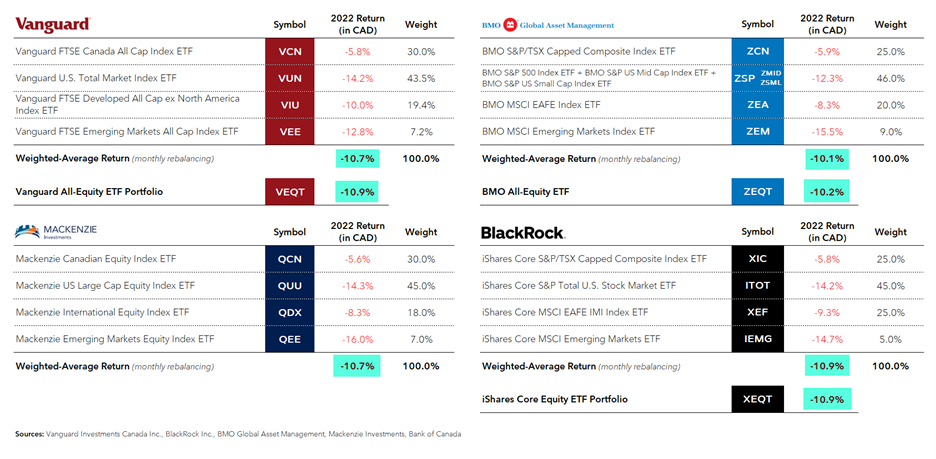

And for those of you invested in all-equity ETFs, like the Vanguard All-Equity ETF Portfolio (VEQT), the BMO All-Equity ETF (ZEQT), and the iShares Core Equity ETF Portfolio (XEQT), you’ll notice their 2022 returns were in line with the weighted-average returns of their underlying ETF holdings.

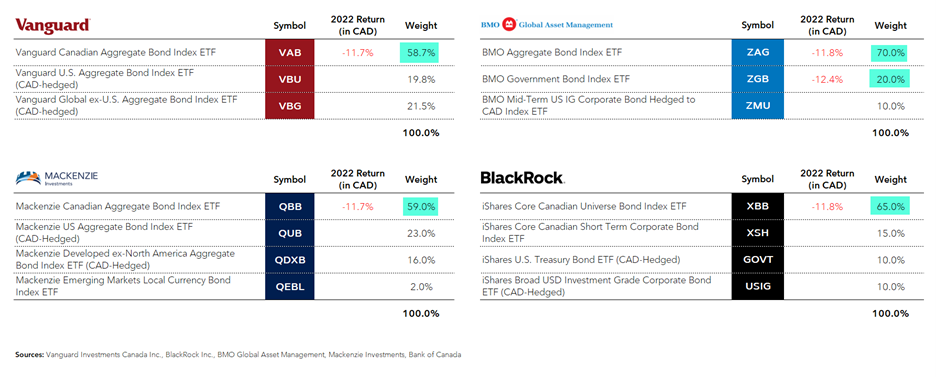

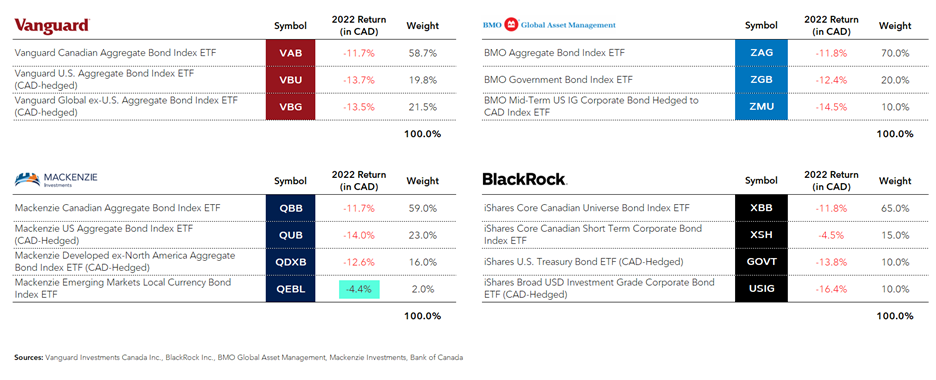

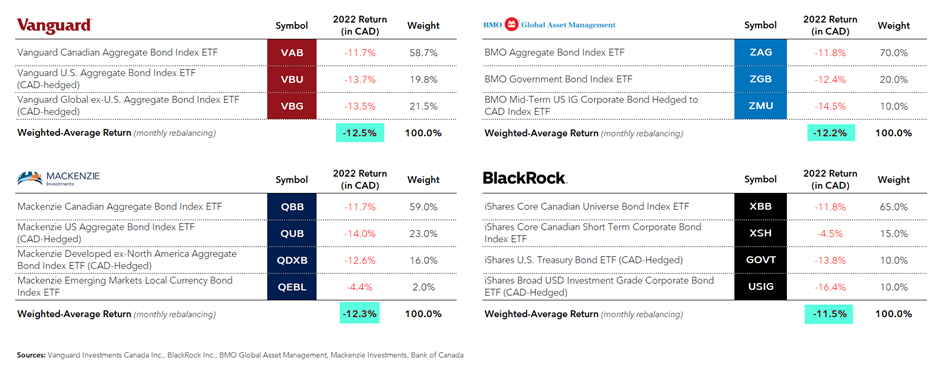

Next, let’s check out fixed income returns, since your asset allocation ETF may hold some bonds too.

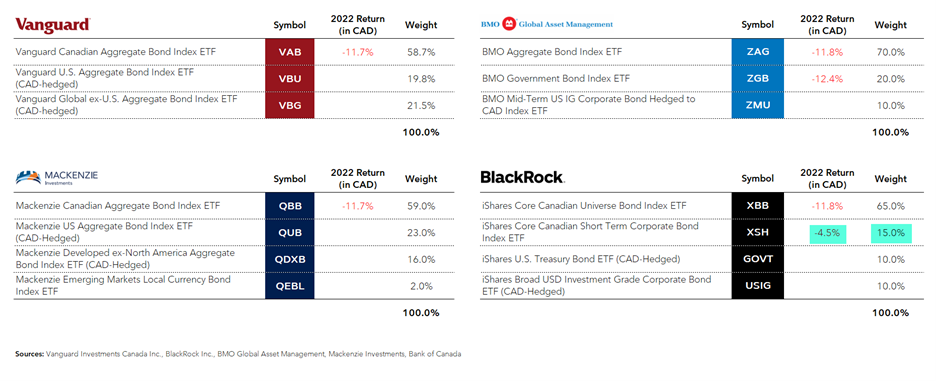

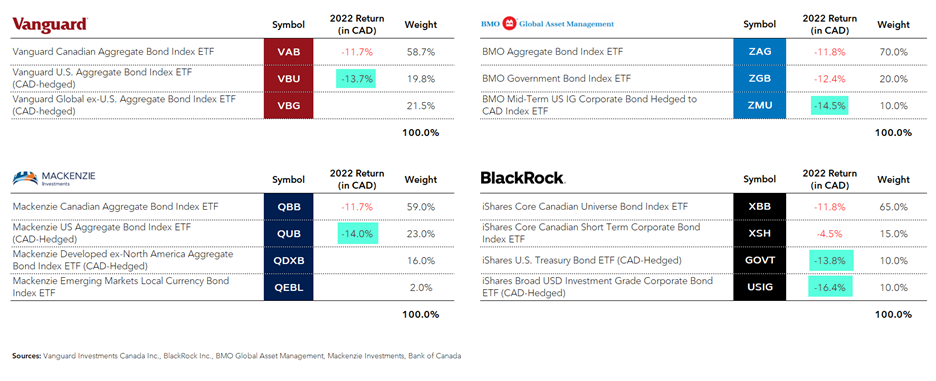

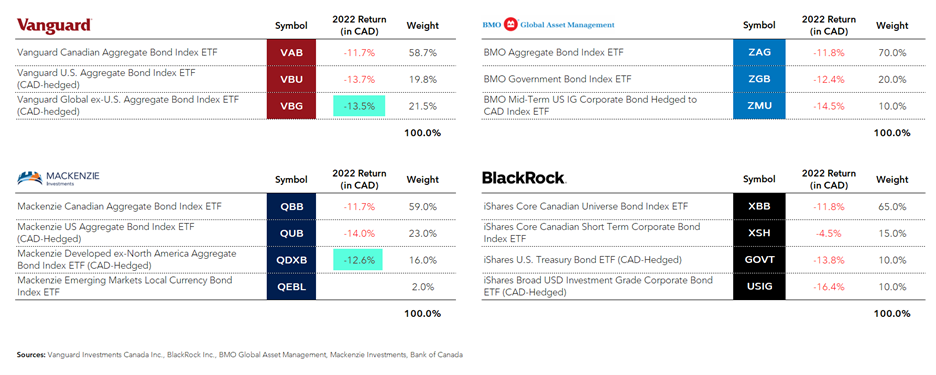

2022 Fixed Income ETF Returns

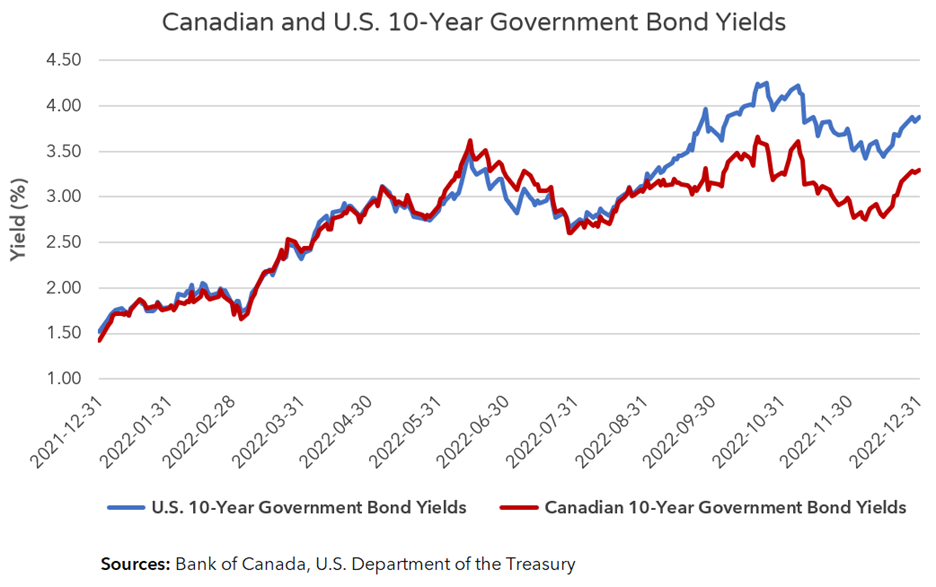

Canadian bond ETFs started the year with a weighted average yield to maturity of 1.9% but had increased to 4.3% by year-end. Remember, an increase in yield decreases bond prices, so this resulted in double-digit losses across most fixed income securities included in these asset allocation ETFs.

Broad market Canadian bond ETFs lost around 12% across the board in 2022. Canadian bonds make up the majority of the fixed income component in these asset allocation ETFs, so they also had the biggest impact on performance.

Short-term Canadian corporate bond ETFs make up 15% of the fixed income allocation of the iShares portfolios. They had less impact, but fared slightly better, with a 2022 loss of just under 5%.

U.S. currency-hedged bond ETFs performed worse than their Canadian counterparts, with negative returns of around 14%–16%.

This was largely because U.S. bond yields diverged from (and rose higher than) Canadian bond yields after the end of August. This in turn drove U.S. bond ETF values lower than Canadian bond ETFs across the same time.

Currency-hedged foreign bond ETFs outside of the U.S. performed similarly to their Canadian and U.S. equivalents, with losses of around 13%.Currency-hedged foreign bond ETFs outside of the U.S. performed similarly to their Canadian and U.S. equivalents, with losses of around 13%.

Local currency emerging markets bond ETFs fared slightly better than currency-hedged developed markets bond ETFs in 2022, losing around 4% in Canadian dollar terms. However, this asset class only makes up a small portion of the Mackenzie Asset Allocation ETFs, so it had little impact on total performance.

All together now: To estimate a ballpark return for each portfolio’s fixed income allocation, we can once again take the weighted average return for each ETF, rebalance monthly, and adjust for the additional fees charged on asset allocation ETFs. Doing so provides us with estimated negative returns of between 11%–13% across the various ETF providers.

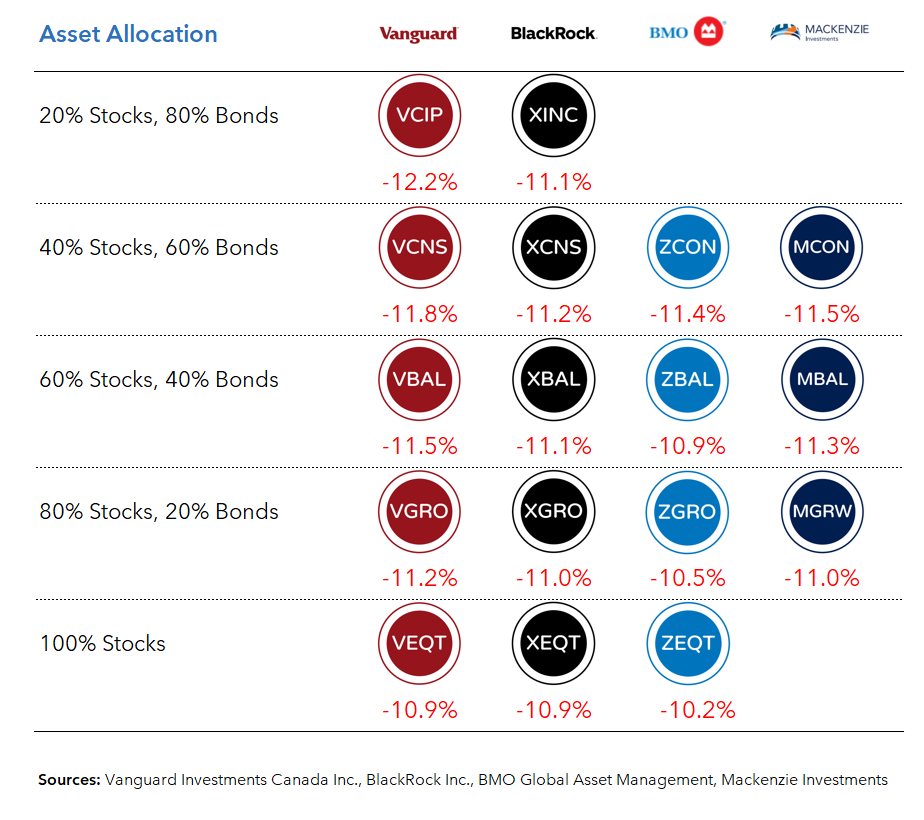

2022 Asset Allocation ETF Returns

Again, it didn’t much matter which asset allocation ETF provider you used in 2022. For nearly every risk level, their returns were within 1% of one another. Since our estimates gave BMO the edge in the equity department, it’s no surprise they squeaked past the others across their balanced, growth, and all-equity allocations. And because the iShares Core Portfolios included better-performing short-term Canadian corporate bonds, they outperformed in the more conservative asset allocation ETFs.

However, as we suggested at the outset, we advise against reading too much into these short-term variations. BMO may have gained a slight edge in 2022, but that doesn’t provide us with any meaningful information on what to expect going forward. Over the long-term, we would continue to expect similar returns for comparable asset mixes.

As always, we advise focusing on what you can control, such as minimizing costs; maintaining asset allocations that align with your personal financial goals; and above all, ignoring the temptation to chase or flee past returns. If anything, 2022’s broad market smack-down positions us for future expected growth moving forward … IF we’re there whenever and wherever it arrives. We hope this year in review offers the perspective you need to invest accordingly.