I know what you’re thinking: “Do we really need another suite of asset allocation ETFs?” Vanguard, iShares and BMO already dominate the marketplace with excellent products, so what could another fund provider possibly have to offer?

Although Mackenzie’s asset allocation ETFs are similar in many ways to the existing offerings from the big 3, they have a few novel features that set them apart from the others. In this blog post, I’ll compare the Mackenzie asset allocation ETFs with the Vanguard, iShares, and BMO portfolios to see how they stack up.

When I first heard of Mackenzie’s asset allocation ETFs, I assumed they were just like the TD One-Click ETF Portfolios – quasi-passively managed funds with an unhealthy dose of active thrown into the mix. Even the prospectus refers to them as the “Mackenzie Balanced Active ETFs”. However, on closer inspection, it turns out Mackenzie’s portfolio managers aren’t given any more leeway than their competitors. The managers have some discretion to adjust and rebalance the portfolios from time to time, but I think it’s safe to place the Mackenzie ETFs into the same passive category as the others.

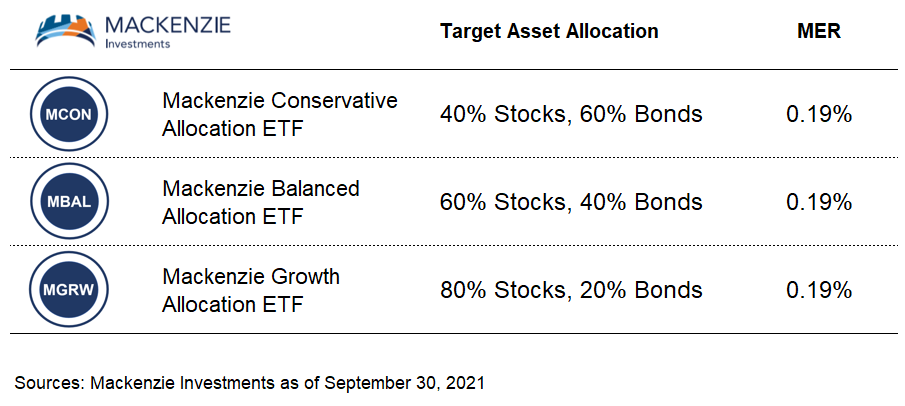

Mackenzie has initially launched three asset allocation ETFs, with options for 40%, 60% and 80% stocks. They all have a management expense ratio (or MER) of 0.19%, which is slightly cheaper than the iShares and BMO portfolios, which charge 0.20%.

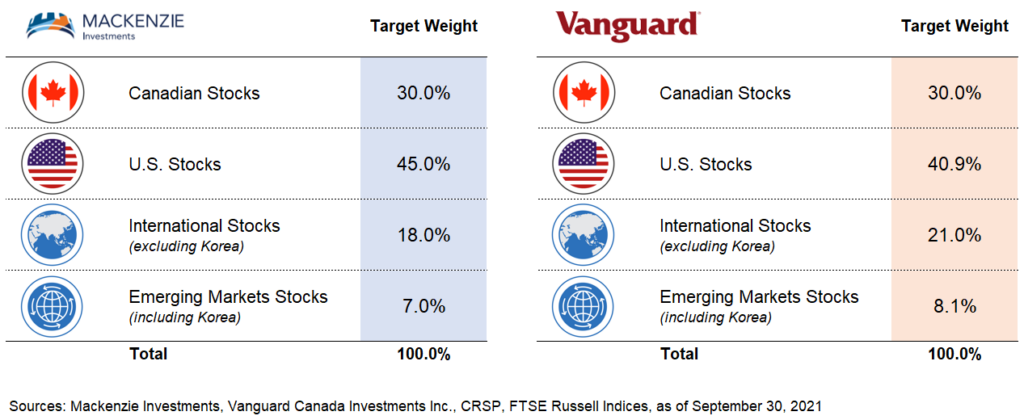

For the equity breakdown, Mackenzie has targeted 30% Canadian stocks and 70% unhedged foreign stocks, which is the same as Vanguard’s split. And although Mackenzie has static target weights for its 70% foreign equity allocation, they are very similar to Vanguard’s current market-cap weights, with Mackenzie’s U.S. equity allocation being slightly higher, and their international and emerging markets a bit lower.

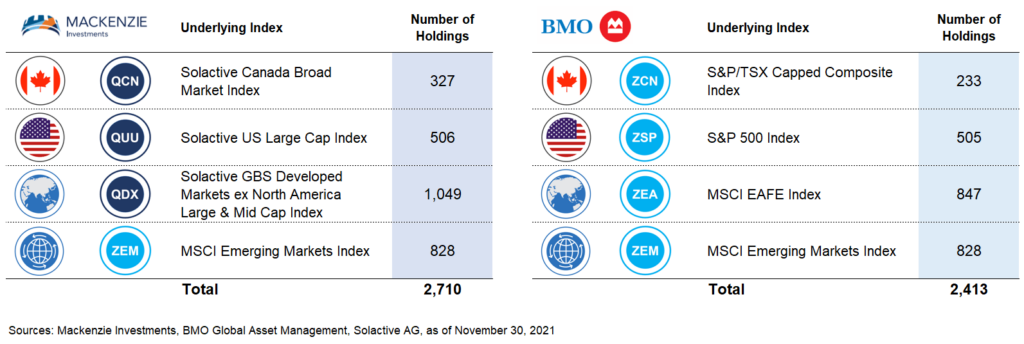

Mackenzie’s portfolios include several underlying equity ETFs that track indexes provided by Solactive. These measure the performance of thousands of companies across the globe.

With about 327 companies, the Solactive Canada Broad Market Index actually contains more small-cap stocks than the benchmarks used by Vanguard, iShares and BMO.

But when it comes to foreign equities, the Mackenzie portfolios are closer to BMO’s, with a focus on large- and mid-cap stocks.

For example, the Solactive US Large Cap Index and the S&P 500 Index both include around 500 large-cap U.S. companies.

On the international equity front, the MSCI EAFE Index and its Solactive counterpart both track the performance of hundreds of large and mid-cap developed companies operating outside of North America.

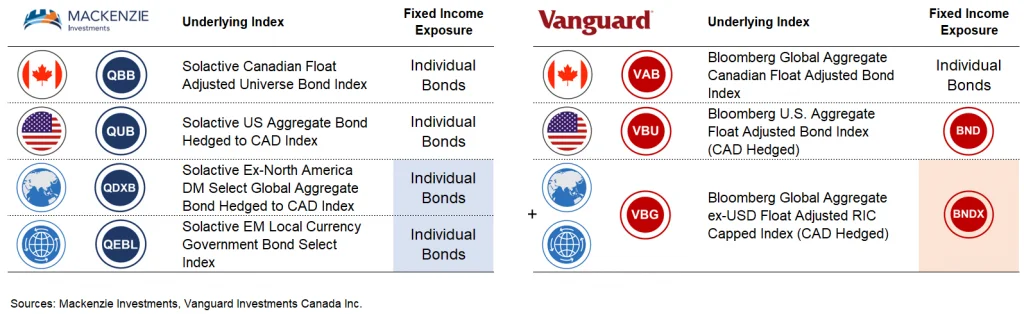

And for emerging markets equity exposure, Mackenzie actually holds the BMO MSCI Emerging Markets Index ETF (ZEM). However, they have filed a preliminary prospectus for the Mackenzie Emerging Markets Equity Index ETF (with ticker symbol QEE) and they plan to replace ZEM once this new fund is launched. QEE will track a Solactive large and mid-cap equity index, and like ZEM, it will also hold the underlying stocks directly, resulting in one less layer of unrecoverable foreign withholding taxes across all account types). This makes QEE more tax-efficient than either of the emerging markets equity ETFs found in the Vanguard or iShares portfolios.

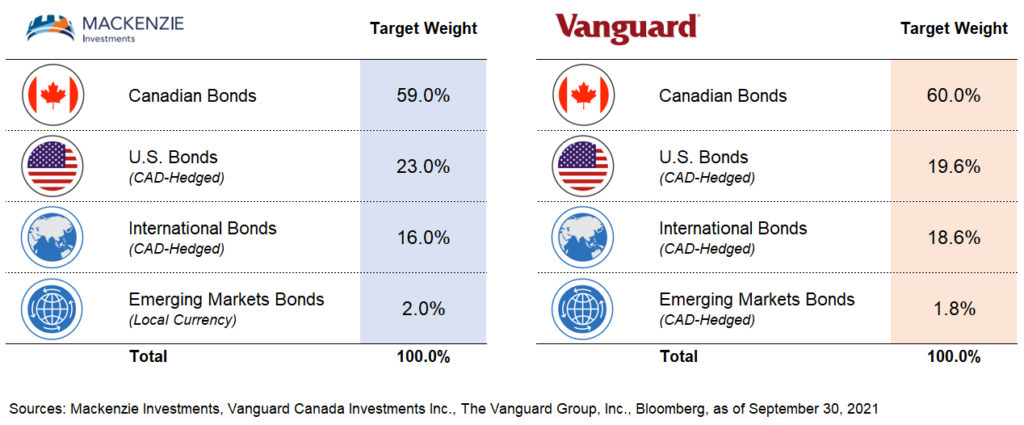

While we’re on the topic of foreign withholding taxes, let’s switch to the fixed income side of the portfolios, where Mackenzie has made several interesting ETF choices to improve tax-efficiency.

In addition to Canadian bonds, Mackenzie also includes U.S., international and emerging markets bonds. The target weights are similar to those found in Vanguard’s portfolios. Here again, Mackenzie’s target weights are static, whereas Vanguard targets a 60% Canadian, 40% foreign bond mix, but allows the regions within the foreign allocation to fluctuate, based on their current market caps.

However, within Mackenzie’s fixed income allocations are two notable differences.

First, Mackenzie has decided to leave the currency exposure of their emerging markets bonds unhedged, whereas Vanguard hedges away the currency risk.

When I asked Mackenzie’s team about their decision, they explained that exposure to emerging markets bonds in their local currency offers a diversification and yield advantage. They also claim that currency has been a key contributor to the total return of local currency emerging markets bonds.

Whatever your preference, this difference is likely to have minimal impact on the fund’s overall returns, as emerging markets bonds make up less than 1% of both the Mackenzie and Vanguard balanced ETF portfolios.

The second difference is much more exciting. Mackenzie has chosen to hold their underlying foreign bonds directly, while Vanguard simply holds U.S.-listed ETFs to gain exposure to these asset classes.

Now, the structure of Mackenzie’s bond funds is not expected to impact the tax-efficiency of the U.S. bonds: treaties between Canada and the U.S. already significantly reduce the amount of U.S. withholding tax applied to interest payments. However, it is expected to eliminate the second layer of 15% U.S. withholding tax applied when a Canadian-listed ETF receives distributions from a U.S.-listed ETF that holds international and emerging markets bonds.

For example, when held in an RRSP or TFSA, Mackenzie’s international and emerging markets bond ETFs, QDXB and QEBL, would only lose one layer of foreign withholding taxes on interest paid from the foreign countries to Canada. By comparison, investors in Vanguard’s international and emerging markets bond ETF, VBG, would be subject to two layers of unrecoverable foreign withholding taxes. This translates into an additional tax drag to VBG investors of around 0.3% per year.

As with our other asset allocation ETF providers, Mackenzie plans to top-up underweight asset classes with any cash flows, so the ETFs should stay close to their targets during most periods. If necessary, the managers will rebalance the portfolios during their quarterly review.

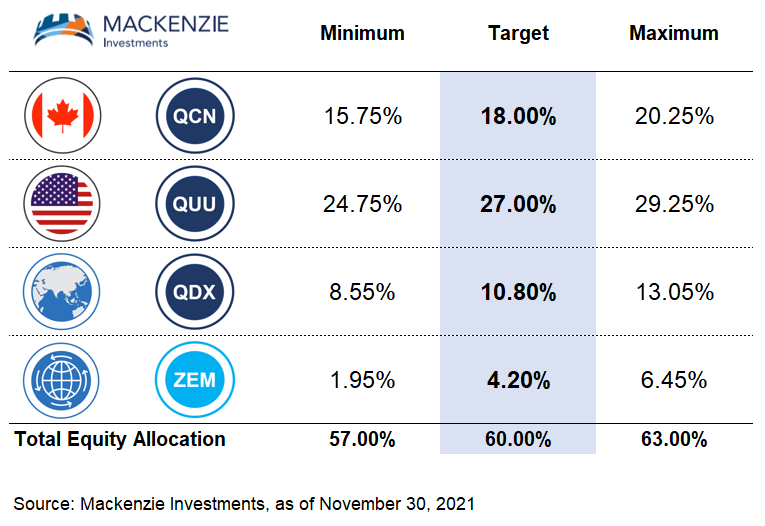

Mackenzie has a 3% absolute rebalancing threshold between the fund’s target equity and fixed income allocations. For example, the Mackenzie Balanced Allocation ETF (with ticker symbol, MBAL), which has a 60% equity target, will be rebalanced if equities have increased to more than 63%, or less than 57%.

As well, the individual asset classes will be rebalanced if they deviate by at least 2.25% above or below their target weights. For example, Canadian equities, which have an 18% target weight in MBAL, will be rebalanced if they increase to at least 20.25%, or decrease to 15.75%.

Overall, the Mackenzie asset allocation ETFs have earned a place alongside their counterparts from Vanguard, iShares and BMO. They even include several new tax-efficient features that make them stand out from their competition. For this reason, I plan to add Mackenzie’s Asset Allocation ETFs to my model portfolios in the new year, so keep an eye out for those.

As well, after hearing about this blog/video, Mackenzie has offered to contribute to SickKids Foundation, so I wanted to take a moment to thank them for this donation.