Hello again, Canadian Portfolio Manager friends. Recently, we took you on an epic odyssey into global currency exposure in your foreign equity ETFs, including these three key takeaways:

All well and good, but this begged an important question:

What if you ONLY want exposure to foreign stock markets, without the potentially damaging currency exposure of unhedged ETFs?

This is where currency-hedged ETFs can be useful. If you could eliminate your foreign currency exposure, you would no longer need to be concerned with its fluctuations, right?

Well, yes, sort of. But, as usual, there are a ton of mind-bending caveats to consider before you decide whether currency-hedged ETFs are the way to go in your own portfolio.

To help you make an informed choice, this new series describes the intricacies of currency-hedged foreign equity ETFs, while covering three more points about them:

We’ll cover all three of these points in our next two posts, or, as usual, you can catch the podcast or YouTube versions here.

How and why does foreign currency hedging work in equity ETFs? We welcome back BlackRock’s Canadian product and capital markets lead Steven Leong to provide an overview:

The purpose of currency hedging is to try to remove fluctuations in an investment’s value due to changes in currency value. Essentially, you’re trying to hedge the risk that your foreign currencies go down against the Canadian dollar by smoothing out currency movement fluctuations and leaving only stock price exposure.

To implement a currency hedge, we typically use instruments known as “forward contracts”. These are derivatives that allow us to sell foreign currency and buy Canadian dollars at an agreed-upon exchange rate today – but where no money actually changes hands until later, typically a month into the future. By locking in a price at which we’re going to sell the foreign currency, if the currency goes down, you’re protected. At the same time, if it goes up, you won’t benefit.

In other words, holding forward contracts lets us balance out the currency exposure from owning foreign stocks. Because these contracts expire, in a currency-hedged ETF, like XUH, we typically set up a hedge at the start of the month, settle the position at month-end, and re-establish a new one in the new month. This is known as “rolling the forwards”, which achieves an uninterrupted hedge against the exposure.

By the way, in this series, we’re focusing on currency hedging for foreign equity ETFs. That’s because the decision for foreign bond ETFs is almost a no-brainer. Volatility is much higher in currency-unhedged vs. currency-hedged foreign bond ETFs. So, especially since bonds should serve as your portfolio’s stabilizing force, we generally recommend hedging 100% of your foreign bond currency exposure. Enough said.

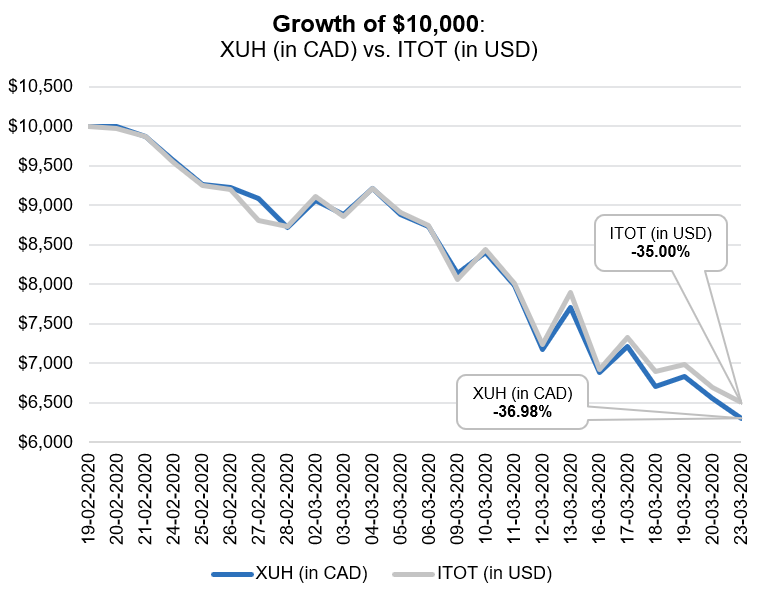

So, to summarize: Currency-hedged ETFs like the iShares Core S&P U.S. Total Market Index ETF (XUH) are trying to provide Canadian investors with returns similar to what a U.S. investor would earn in the same U.S. market – but without any U.S. dollar exposure drama.

However, there have been times when XUH did not closely follow U.S. stock market returns. For example, from February 19 – March 23, 2020, the U.S. stock market lost 35% of its value. The unhedged iShares Core S&P Total U.S. Stock Market ETF (ITOT) also lost 35% in local currency returns. But the currency-hedged equivalent, XUH, lost 37% of its Canadian dollar value. It lagged the U.S. stock market’s local currency return by 2% over this brief period.

Steven explains:

Currency-hedging doesn’t perfectly eliminate all currency exposure, partly because the hedge is being reset monthly. During any given month, foreign stocks rise and fall a bit, which makes the hedge slightly too large or too small relative to those stocks. However, monthly hedging usually strikes a good balance between adjusting too often and too little. While currency forward trade costs are generally inexpensive, they could still add up if you trade too often. Short-term interest rates also affect how currency forwards are priced, so this introduces a bit of noise into hedged ETF performance.

I want to stress: A fund manager can’t simply make currency exposure disappear. We actually have to transact in financial instruments to implement a hedge. Just as there is no magic “minimize tracking error” button, there’s no magic “hedge currency” button.

As we’ll explore further in our next post, we include only unhedged foreign equity ETFs in our CPM model portfolios. But as Steven says, “There are a lot of good and popular options for investors who either have a strong view on the Canadian dollar, or would simply prefer to avoid currency ups and downs.”

If that sounds like you, you could easily swap out any of the U.S. and international equity ETFs in our CPM portfolios with currency-hedged Canadian-based alternatives. Product costs and foreign withholding taxes would be similar either way.

From BlackRock, there’s the aforementioned XUH, which delivers the same stock exposure as the unhedged iShares Core S&P U.S. Total Market Index ETF (XUU).

For international exposure, iShares Core MSCI EAFE IMI Index ETF (XEF) has a hedged cousin that trades under the ticker XFH. According to Steven, “XFH actually has to hedge 12 different currencies. The yen and the euro are the largest, and the New Zealand dollar and the Israeli shekel are the smallest, at only a half-percent each.”

In addition, BlackRock’s CAD-hedged iShares Core S&P 500 Index ETF (XSP) was the world’s first currency-hedged ETF. “Canadians are pioneers in the currency-hedged ETF space,” says Steven. “This was partly because our own currency is fairly volatile, and partly because of our history of imposing foreign content limits. XSP was created in the mid-2000s to deal with those issues, and it’s still going strong today.”

Vanguard Canada also has currency-hedged equivalents for the U.S. and international equity ETFs found in the CPM model portfolios. VUS is the currency-hedged version of the Vanguard U.S. Total Market Index ETF (VUN), and VI is the currency-hedged version of the Vanguard FTSE Developed All Cap ex North America Index ETF (VIU).

Neither Vanguard nor BlackRock offer currency-hedged versions of their emerging markets equity ETFs. In its 2014 paper, “To hedge or not to hedge?” Vanguard suggests why: “Unlike most major developed-market currencies, emerging-market currencies tend to have lower trading volumes and may be more difficult and costly to hedge.”

We’ve now described the lay of the land for currency-hedged equity ETFs. In our next post, we’ll zoom in for a closer look at why Canadians must consider currency hedging from an unusual risk-and-return perspective. This also explains why we use unhedged equity funds in our CPM model portfolios.

Intrigued? We’ll be back soon with more information.