By now, you’re probably getting the hang of how to handle foreign withholding taxes, based on our past blog/video on international equity ETFs. But complex lessons bear repeating. So, this time, let’s take what you’ve learned on foreign withholding taxes, and apply it to emerging markets equity ETFs.

Recall that the amount of withholding tax payable on foreign dividends depends on two important factors:

The first is the structure of the ETF that holds the stocks. The second is the account type in which you’re holding the ETF. By account type, we’re talking about whether the ETF is an RRSP, TFSA, non-registered account, and so on.

Depending on these two factors – structure and account type – the foreign dividends on your emerging markets stock ETF could be subject to one, or even two layers of withholding tax.

Level I withholding taxes are those levied by the developing countries where the companies are domiciled, such us China, Brazil, and so on.

Level II withholding taxes are incurred when the emerging markets stocks are held indirectly via a U.S.-listed ETF. In some account types, there’s an additional 15% U.S. withholding tax on foreign dividends before the U.S.-listed ETF pays the net dividends to Canada.

With this in mind, let’s look at foreign withholding taxes for the emerging markets equity ETFs we introduced in our last lesson:

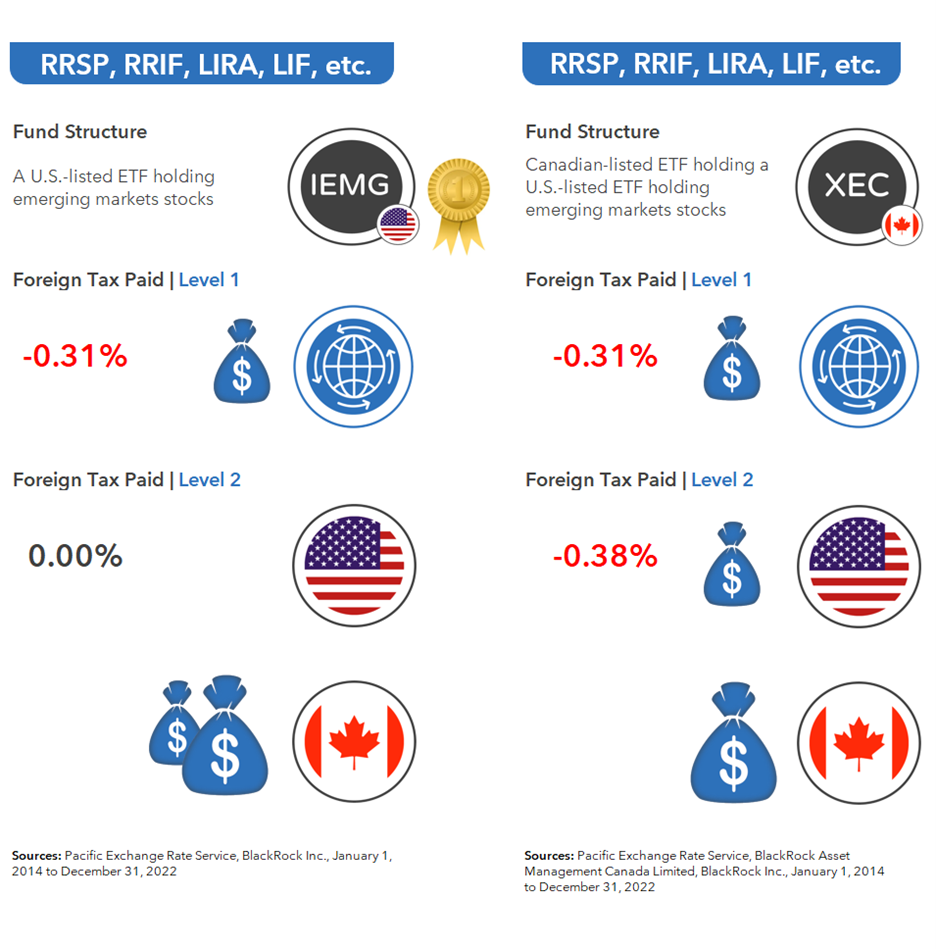

In terms of fund structure, VWO and IEMG are considered U.S.-listed ETFs that hold emerging markets stocks. VEE and XEC are Canadian-listed ETFs that hold U.S.-listed ETFs that hold emerging markets stocks.

When held in an RRSP or RRIF, funds such as XEC or VEE are subject to two layers of foreign withholding taxes. That’s because they are Canadian-listed ETFs that gain their exposure to emerging market stocks by holding a U.S.-listed ETF. The first layer of withholding tax occurs when the foreign companies pay dividends to the U.S. The second layer is levied when the foreign dividends are paid from the U.S. to Canada. Since January 1st, 2014, the combined level 1 and level 2 foreign withholding tax drag has been substantial.

In contrast, U.S.-listed emerging markets equity ETFs, like IEMG or VWO, still incur the first level of withholding tax when the foreign companies pay dividends to the U.S. However, this structure is exempt from the second 15% layer of U.S. withholding tax when held in an RRSP or RRIF. As we’ve mentioned in the past, that’s due to a tax treaty between Canada and the U.S. And, at least from the perspective of reducing foreign withholding taxes, this makes IEMG and VWO superior choices for your RRSP or RRIF.

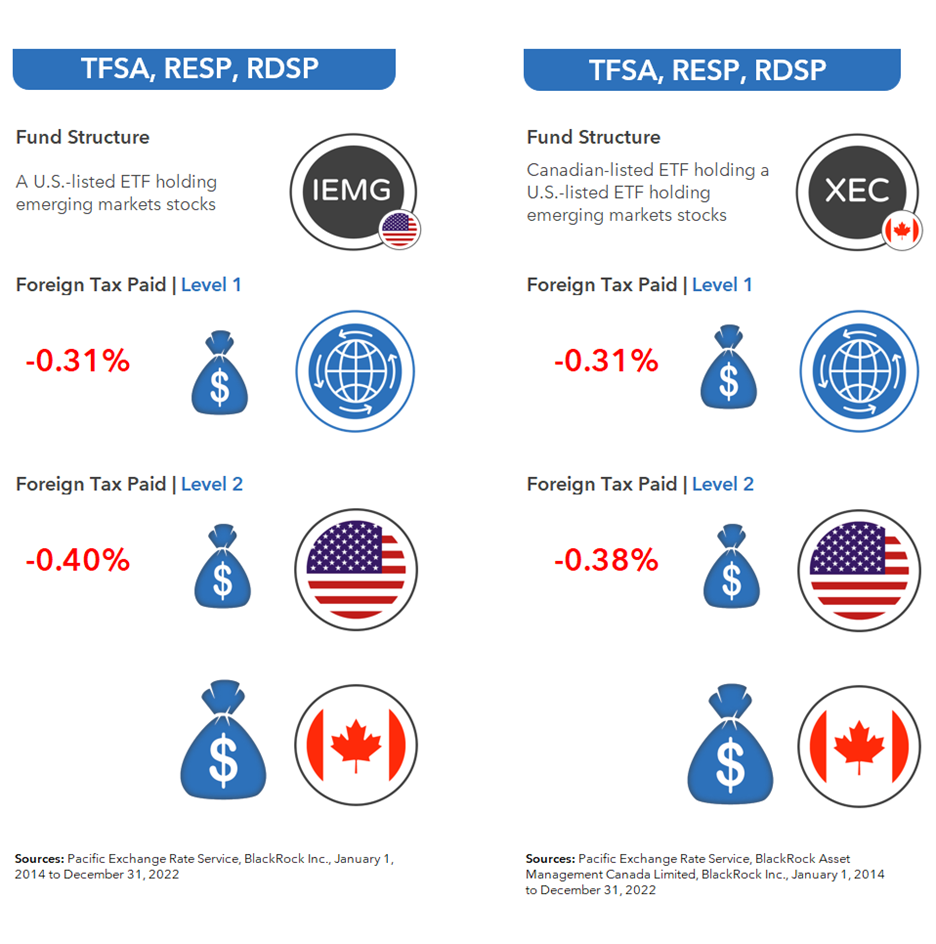

What if you’re holding emerging markets equity ETFs in TFSA, RESP, and RDSP accounts? No tax treaty exists between Canada and the U.S. to exempt the 15% U.S. withholding tax in these account types. So, regardless of the structure, your investment will be subject to two similar layers of foreign withholding taxes. Again, strictly from a foreign withholding tax perspective, it doesn’t matter which fund you choose.

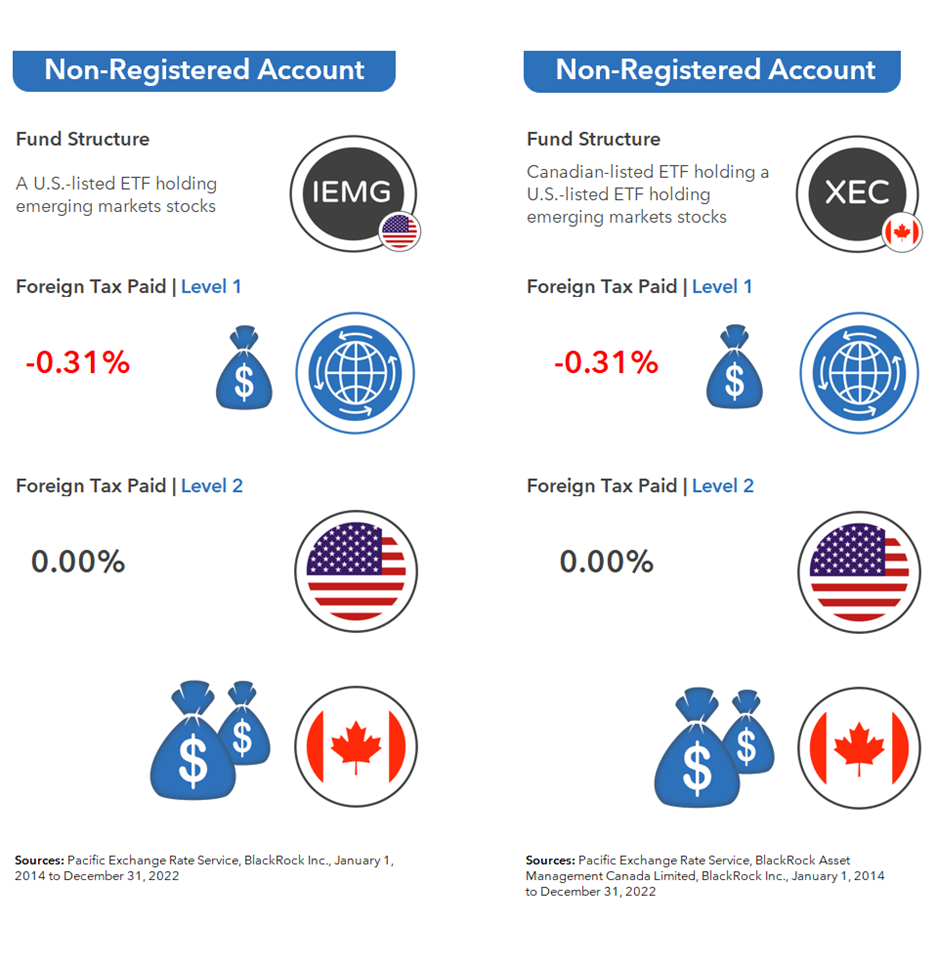

Last, let’s look at holding emerging markets ETFs in your non-registered accounts.

When you hold a Canadian-listed ETF like XEC or VEE—which holds a U.S.-listed ETF that holds emerging markets stocks—both layers of withholding taxes will apply – although the second layer of U.S. withholding tax is generally recoverable each year when you file your tax return.

For a U.S.-listed ETF, like IEMG or VWO—which directly holds the emerging markets stocks—the foreign dividends are also subject to two layers of withholding taxes, and, again, the second layer of U.S. withholding tax is generally recoverable.

So, for foreign withholding taxes in non-registered accounts, neither fund structure has an advantage over the other.

Once again, this foreign withholding tax material can be tricky, so feel free to review the content again if the concepts have got you stumped. In our next blog/video, we’ll review the impact of currency conversion fees when buying or selling U.S.-listed emerging markets equity ETFs. See you then!