Hi Justin – this is Mark H from Edmonton. PWL Capital recently published a white paper on how to estimate future stock and bond returns. Using the same methodology, what are the expected returns for the Vanguard Asset Allocation ETFs, in terms of both the expected premium above inflation, and the expected return including inflation.

Bender: Hi, Mark. Thanks for sending in your question, which I’m certain will appeal to many readers. I hope you won’t mind: When collecting the data, I’ve strayed slightly from the PWL methodology by referencing online resources anyone can access. This will allow investors to recreate their expected portfolio returns whenever they please, using the following six steps.

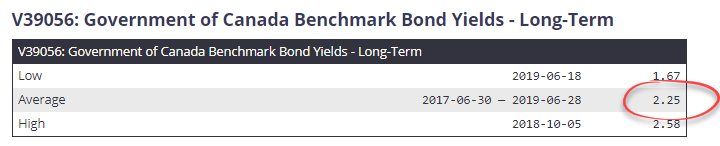

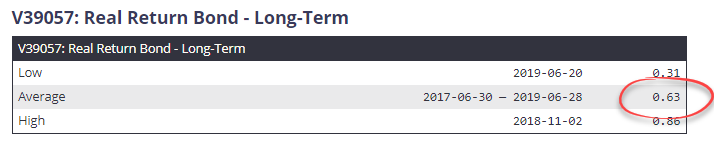

For this figure, we’ll head to the Bank of Canada website, where we can compare the yield of a long-term Government of Canada notional bond (which includes an inflation expectation) with the yield of a real return bond of similar maturity (which excludes inflation). The difference between these two figures provides us with the market’s ballpark estimate of future inflation. Similar to the PWL white paper, we’ll remove any short-term yield discrepancies by using the 24-month average of the yield difference between them. As of June 28, 2019, the average difference, or long-term inflation expectation, was around 1.6% (2.25% – 0.63%).

Now that we have our future inflation expectation, we’ll estimate Canadian and global stock market returns over the next 10–15 years.

Forecasting long-term stock returns is a bit of a mug’s game. Vanguard published a paper in 2012 where they examined 15 metrics to determine whether any of them had the ability to predict future stock returns. They found the most predictive power in valuation metrics such as price-to-earnings (P/E) ratios. But they were only meaningful over long time horizons, and even then, the P/E ratios only explained the variation in real stock returns about 40% of the time.

The best valuation metric examined in the study was the cyclically adjusted P/E ratio. Also known as the Shiller CAPE ratio, it was named after Nobel laureate and Yale Professor of Economics Robert Shiller. The CAPE ratio takes a stock’s current value and divides it by the average inflation-adjusted company earnings over the previous 10 years. A 10-year period is used to ensure that profits are averaged over more than one earnings cycle; the inflation adjustment ensures that company profits are still comparable, even during periods of high inflation.

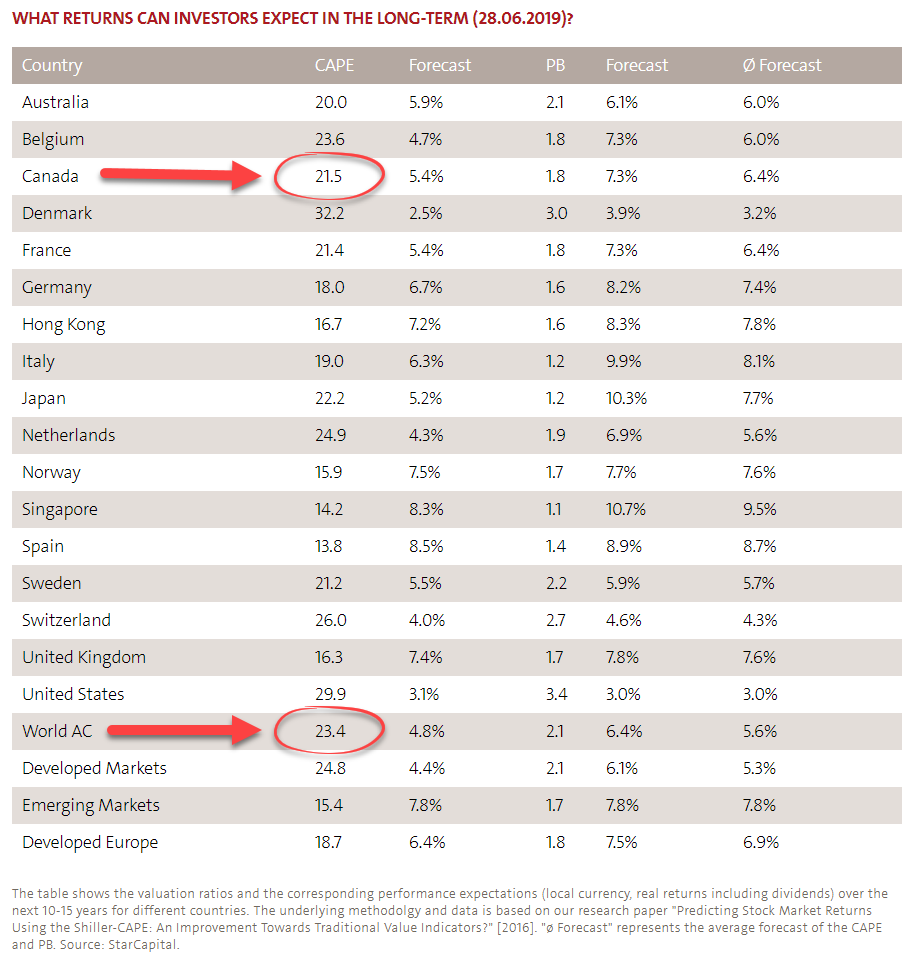

StarCapital publishes monthly global CAPE ratios for various equity regions, so I’ve used these CAPE figures for our analysis. We can obtain an earnings yield for any given stock market by taking the inverse of its CAPE ratio (which means dividing 1 by the CAPE). This can be thought of as a stock market’s expected real return. As these are real return expectations, we’ll still need to add in our 1.6% inflation expectation, so we can accurately compare them to the notional returns reported on your investment account statements.

As of June 28, 2019, the Canadian stock market had a CAPE of 21.5. Dividing 1 by the CAPE gives us an expected real return of 4.7%, or an expected nominal return of 6.3% after adding in our 1.6% expected inflation.

The global stock market (“World AC” on the StarCapital site) has a CAPE of 23.4. Dividing 1 by the CAPE gives us an expected real return of 4.3%, or an expected nominal return of 5.9% after adding in our 1.6% expected inflation.

So, Canadian stocks are expected to return 6.3% over the next 10–15 years, and global stocks are expected to return 5.9%. If these figures seem low to you, remember they come after a decade of incredible performance, when global stock markets returned an annual average of +12% in Canadian dollars.

| Asset Class | Country | CAPE | Expected Real Return (1 ÷ CAPE) |

Expected Inflation | Expected Nominal Return |

|---|---|---|---|---|---|

| Canadian Stocks | Canada | 21.5 | 4.7% | 1.6% | 6.3% |

| Global Stocks | World AC (All Country) | 23.4 | 4.3% | 1.6% | 5.9% |

It’s also interesting to note that the U.S. stock market has an even higher CAPE of 29.9, indicating low future real and nominal annual expected returns of only 3.3% and 4.9% respectively. This is no surprise, as the U.S. stock markets have been on a tear for the past ten years, delivering an annual average return of +16% in Canadian dollars. While you should not use these lower future expected returns to engage in market-timing, they could further justify a generally sound approach to diversifying your equity holdings beyond just the U.S.

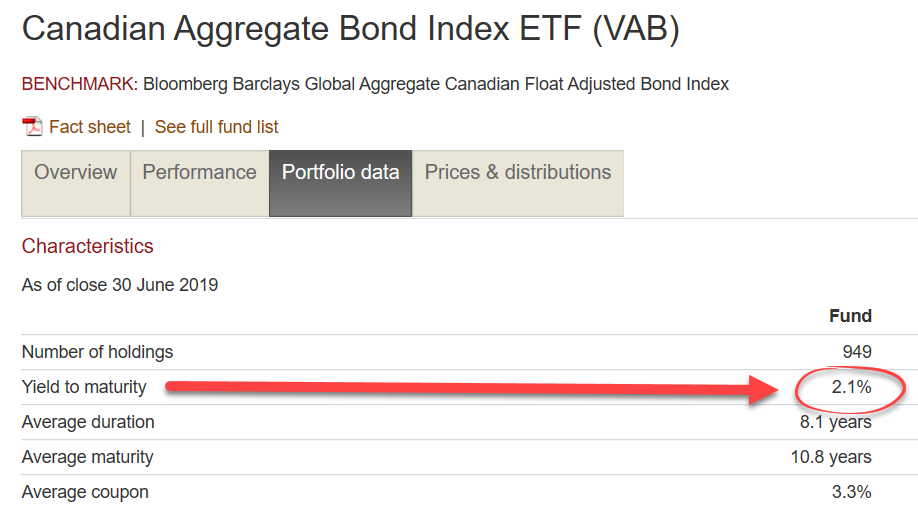

If lower future expected stock market returns have got you down, prepare to be even more disappointed with your bonds. For the Canadian bond portion of the Vanguard Asset Allocation ETFs, the underlying bonds’ average yield to maturity (YTM) is our best estimate. This average sits at a meager 2.1% as of the end of June 2019.

The Vanguard Asset Allocation ETFs also include currency-hedged foreign bonds, and it’s a bit more complicated to estimate their expected returns. If we simply used their current YTM, U.S. bonds would be expected to return 2.5%, and international bonds would be expected to return only 0.7%. But currency-hedged global bond ETFs are also expected to provide a “hedge return” from the return on their currency-hedging strategies.

Fortunately, I’ve already done the heavy lifting on that calculation in a recent blog post, which I encourage you to revisit. Once the additional returns are factored in, global bonds currently have an adjusted YTM of around 1.9%. If you no longer had this data moving forward, you could get away with just assuming the currency-hedged global bonds are expected to return the same as Canadian bonds, or currently around 2.1%.

Whether you invest within a TFSA, RRSP or taxable account, your Vanguard Asset Allocation ETF will be subject to foreign withholding taxes, creating an additional drag on your returns. When you hold your ETF in a taxable account, you’ll receive a T3 slip at tax time indicating the amount of foreign tax that you’ve already paid. This acts as an “IOU” from the tax collector, which is a good thing. When you hold your ETF in a TFSA or RRSP, you receive no T3 slip, so the foreign withholding taxes you’ve paid are lost forever.

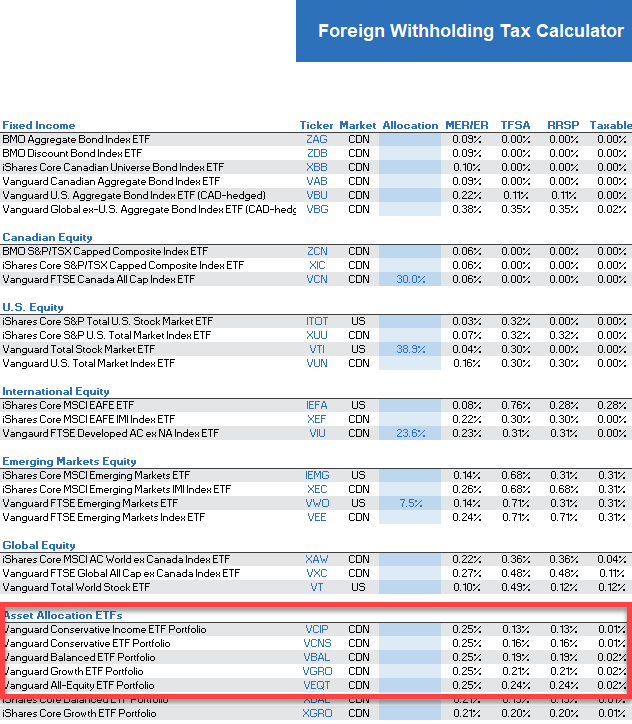

In TFSA and RRSP accounts, the annual tax drags are lower for the more conservative ETFs. They range from as low as 0.13% for the (VCIP), to as high as 0.24% for the Vanguard All-Equity ETF Portfolio (VEQT). If you’re interested in estimating the foreign withholding drag of each asset allocation ETF, you can download the Foreign Withholding Tax Calculator, available on my Canadian Portfolio Manager blog.

Once you add in the 0.25% MER for Vanguard’s Asset Allocation ETFs, annual costs increase in the range of 0.38% for the most conservative asset allocation ETF, to around 0.49% for the most aggressive.

After we adjust each asset class return for its weight within the asset allocation ETFs, and we decrease them by their product fees and foreign withholding taxes, we end up with the following expected nominal return figures.

| VCIP | VCNS | VBAL | VGRO | VEQT | |

|---|---|---|---|---|---|

| Nominal Expected Return | 2.4% | 3.2% | 3.9% | 4.7% | 5.5% |

The real returns (after inflation) are even less exciting, ranging from 0.8% for the most conservative ETF, to 3.9% for the 100% equity ETF.

| VCIP | VCNS | VBAL | VGRO | VEQT | |

|---|---|---|---|---|---|

| Real Expected Return | 0.8% | 1.6% | 2.4% | 3.1% | 3.9% |

All this said, as we suggested at the outset, the future is uncertain. Highly uncertain. It’s important to keep that in mind when considering expected returns, even over the long-term. Over the next 10–15 years, actual returns on these asset allocation ETFs (and any other investments) could vary widely from our rough estimates.

Perhaps the key takeaway from all these calculations is as follows. Even with an all-equity portfolio, you’re probably best off if you don’t expect years and years of double-digit returns going forward. At the same time, we’ve enjoyed a solid ride for the past decade, which may or may not last for a while longer. Who knows?

In the face of eternal uncertainty about what the future has in store, the wise investor builds an efficient, globally diversified portfolio that reflects their personal long-term goals and reasonable expectations about what markets have to offer. Then they sit tight for the ride.